Download the full study (PDF). 92 pages: ranking of 20 banks, key findings, and methodology.

What this study is about

The digital maturity of a business banking app is how quickly, conveniently, and securely a company solves everyday tasks in it: payments, lending, acquiring, employee access, and analytics. We evaluated 20 business apps present in the Uzbekistan market across 110 parameters and compiled a picture of where the market is already strong and where it still noticeably lags behind.

How we measured

- Object: mobile and web applications for corporate clients and small and medium-sized enterprises (SME).

- Scope: 20 apps, 110 parameters.

- Structure: parameters are grouped into 12 digital maturity directions (below). For each direction, we looked not only at the presence of a feature but at how much it actually saves the client's time.

- Evaluation logic: apps were compared with market leaders in terms of convenience and completeness of scenarios — from a simple "feature exists" to "how much it saves the client's time."

Digital maturity directions

| Direction | What was evaluated |

|---|---|

| Customer service | Support channels, issue resolution speed, self-service |

| Payments and autopayments | Speed and automation of regular payment operations |

| Corporate lending | The "from application to money" journey, online processing |

| Acquiring and payment acceptance | Integration of payment acceptance into business processes |

| Open APIs | Ability to embed the bank into business systems |

| Analytics and dashboards | Transition from statements to predictive analytics |

| Access management and roles | Flexibility of the role model for the team |

| Cybersecurity | Corporate data protection standards |

| Non-financial services | The bank's value as a business growth partner |

| Single window for business | Services around the account: from LLC registration to counterparty verification |

| Regional availability | Operation of services outside the capital |

| UX/UI | Interface convenience as a tool to save the client's time |

A breakdown of each direction is in the materials below.

Key findings

- High maturity contrast. The market is developing unevenly: some banks have legacy-level interfaces, while others have implemented modern products.

- Dominance of the payment contour. Banks are accelerating mass operations, but the development of other services is lagging.

- Focus on the basics. Banks are strong in the fundamentals but hardly differ from each other and are not ready for AI and Open Banking.

- Potential of integrations and analytics. Full integrations with external systems are offered only by a few banks; the majority are limited to basic reports without deep analytics.

- Unrealized demand for non-financial services. Education, consulting, and B2B services are minimally developed.

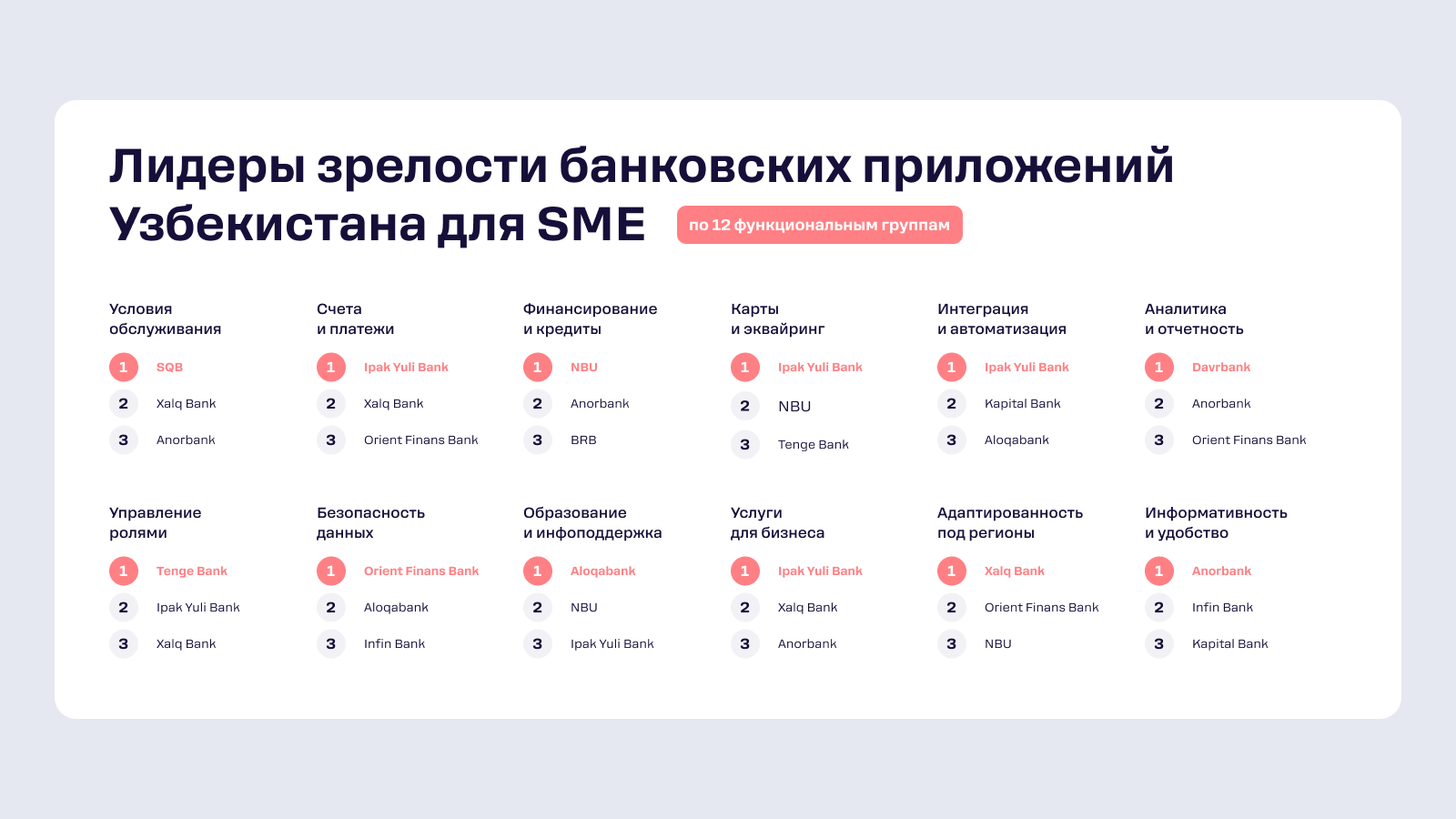

Leaders across 12 directions

According to the Rocket Tech study — the top 3 banks in each direction of SME app digital maturity:

| Direction | 1st place | 2nd place | 3rd place |

|---|---|---|---|

| Terms of service | SQB | Xalq Bank | Anorbank |

| Accounts and payments | Ipak Yuli Bank | Xalq Bank | Orient Finans Bank |

| Financing and loans | NBU | Anorbank | BRB |

| Cards and acquiring | Ipak Yuli Bank | NBU | Tenge Bank |

| Integration and automation | Ipak Yuli Bank | Kapital Bank | Aloqabank |

| Analytics and reporting | Davrbank | Anorbank | Orient Finans Bank |

| Role management | Tenge Bank | Ipak Yuli Bank | Xalq Bank |

| Data security | Orient Finans Bank | Aloqabank | Infin Bank |

| Education and info support | Aloqabank | NBU | Ipak Yuli Bank |

| Business services | Ipak Yuli Bank | Xalq Bank | Anorbank |

| Regional adaptability | Xalq Bank | Orient Finans Bank | NBU |

| Informativeness and convenience | Anorbank | Infin Bank | Kapital Bank |

Frequently asked questions

What is the digital maturity of a business banking app? It is a comprehensive assessment of how well an app covers a company's real tasks — payments, lending, employee access, analytics — quickly, conveniently, and securely, rather than just formally supporting a feature.

How many apps and parameters were evaluated? 20 business banking apps in Uzbekistan across 110 parameters, grouped into 12 maturity directions.

Who conducted the study? The research department of Rocket Tech — a team that designs and implements digital products for banks and fintech companies: from UX and mobile apps to integrations and process automation.

Full study

Detailed data and methodology are in the full version of the Rocket Tech study.