There is a noticeable gap between conservative banking products and the real e-commerce tools businesses use every day. Acquiring is ceasing to be just a "terminal at the checkout" and must evolve into a flexible sales infrastructure embedded in the client's business model. A study on the digital maturity of SME banking in Uzbekistan shows where this gap is particularly wide.

📄 Download the full study (PDF) — data on 20 banks in Uzbekistan across 110 parameters, maturity rating, and methodology.

The Short Answer

Mature acquiring is when payment acceptance is seamlessly built into the client's business model: online onboarding, support for subscriptions and QR codes, and digital cards with limits. For now, onboarding remains a technical quest, while recurring payments and category limits are in short supply. "Invisible" acquiring is the kind that doesn't hinder sales and doesn't force the client to think about the bank behind the checkout.

Why Acquiring Must Become "Invisible"

A business's customer pays without thinking about which bank is behind the checkout—and rightly so. The less noticeable acquiring is in the purchase scenario, the higher the sales conversion. For the business itself, "invisibility" means something else: onboarding without bureaucracy, accepting payments in any channel (checkout, website, messenger), and clear, predictable fees.

Acquiring today is not a device, but an infrastructure layer. And the winning bank is the one whose layer is easiest to integrate into how the business already sells.

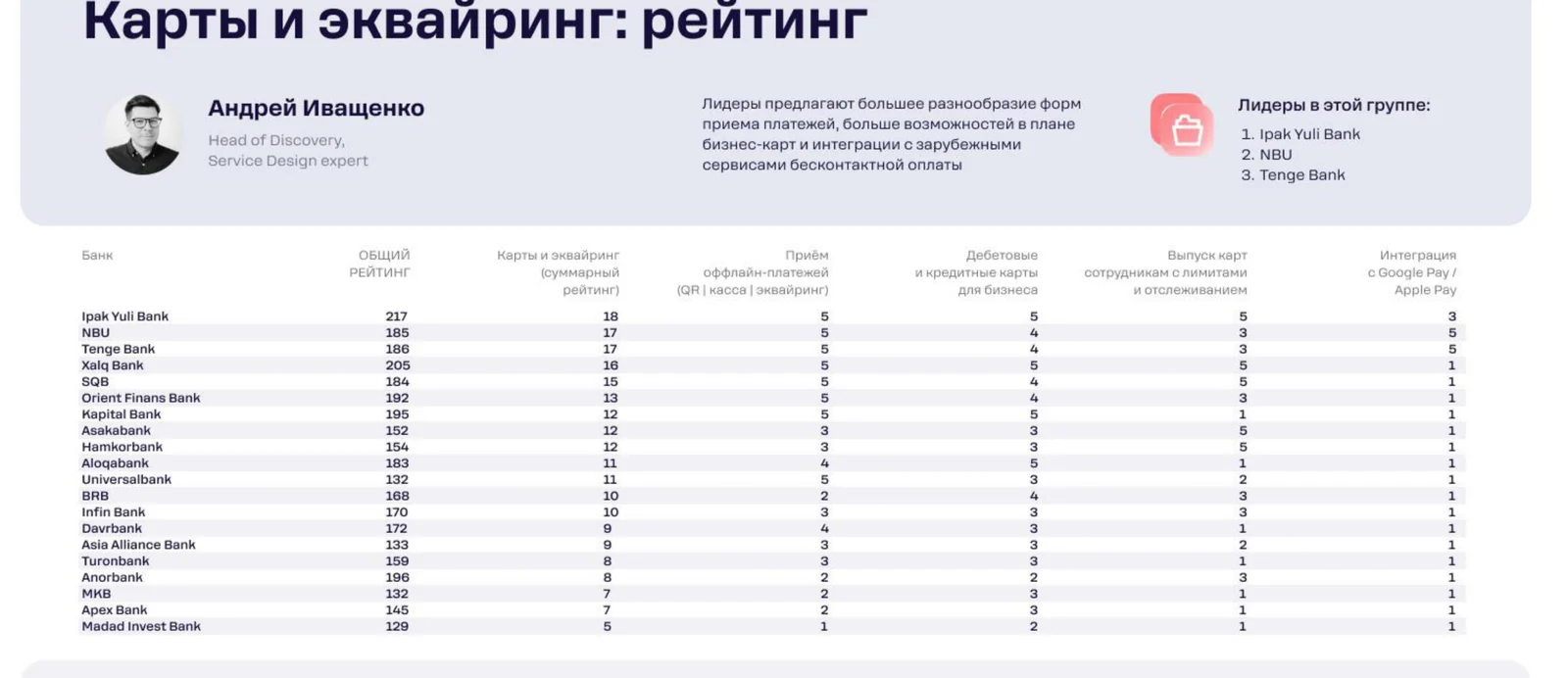

What the Study Showed

Category leaders according to the Rocket Tech study ("Cards and Acquiring"): 1. Ipak Yuli Bank, 2. NBU, 3. Tenge Bank.

<!-- smeuz-fig:m08_ekvayring_rating start -->

Cards and acquiring rating: online onboarding, subscriptions/QR, and corporate cards are more developed among the leaders.

<!-- smeuz-fig:m08_ekvayring_rating end -->The market's growth points show that acquiring is still perceived as "hardware" rather than a service.

Complex Onboarding

In many banks, onboarding remains a technical quest without the option of online registration and with opaque fee calculations.

Weak Support for Modern Scenarios

Recurring (subscription) payments and instant QR payments have limited support, even though they form the foundation of modern business models.

Deficit of Digital Cards

Corporate cards with spending category limits are scarce on the market, and without them, it is difficult for businesses to control employee expenses.

How It Looks in Practice

A small online store wants to accept payments on its website and sell subscriptions. In an immature bank, connecting acquiring means submitting an application, waiting, visiting a branch, and dealing with unclear fees, while recurring charges have to be invented from scratch. The launch is delayed for weeks. In a mature scenario, the store connects acquiring online, sees transparent fees, embeds a ready-made SDK into the website, and launches the subscription in a day. Payments via QR and on the website work equally smoothly, and corporate cards with limits allow issuing advertising budgets to employees without manual reconciliation. Sales start when the business is ready for them, not when the bank finishes the paperwork.

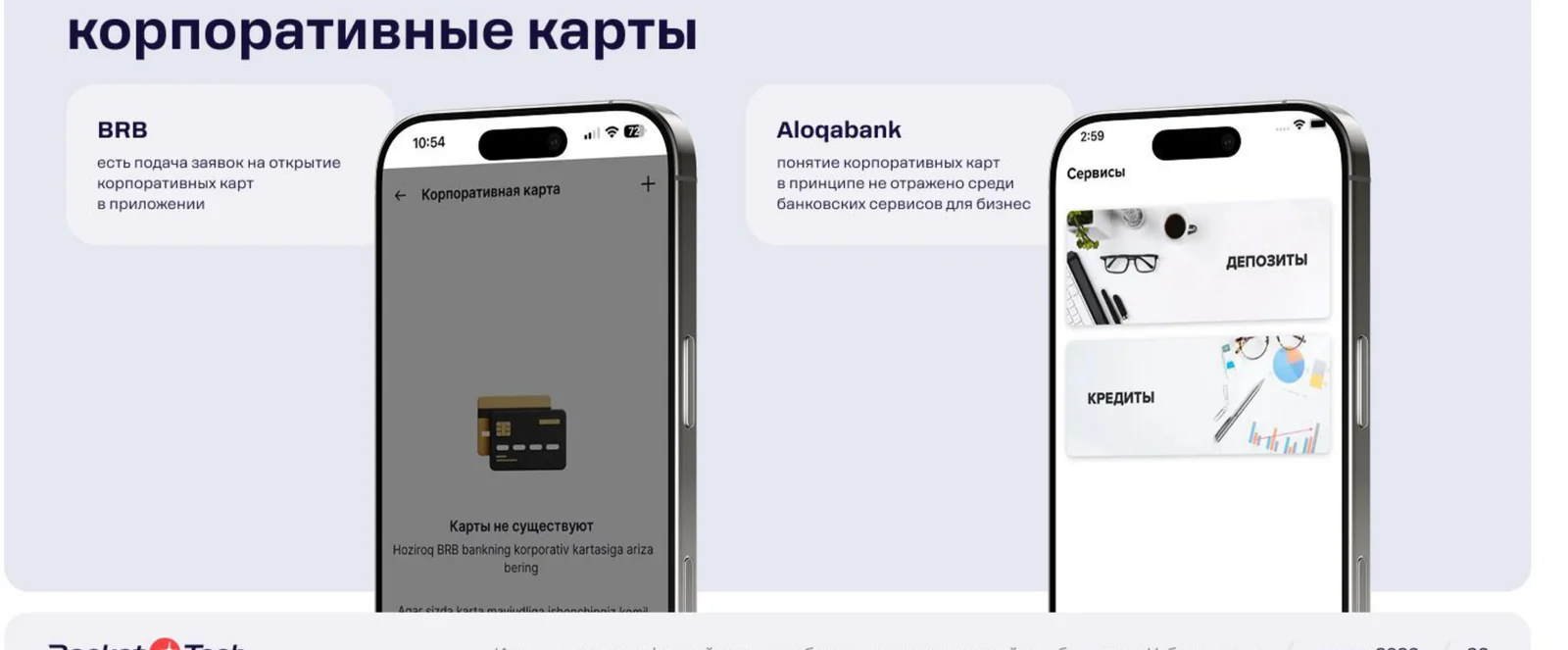

<!-- smeuz-fig:m08_ekvayring_screens start -->

BRB allows applying for a corporate card directly in the app. Aloqabank's corporate cards come with spending category limits.

<!-- smeuz-fig:m08_ekvayring_screens end -->How It Is Solved

- Online acquiring registration with transparent fee calculations and integration with popular marketplaces.

- APIs and SDKs to support the subscription sales model and embed payments into the business's own channels.

- Digital business cards with category limits and direct integration into ERP systems.

It is exactly this integration layer—APIs, SDKs, embedding payment acceptance into client checkouts, websites, and ERPs—that Rocket Tech designs and implements for banks and fintech products: so that acquiring can be connected online and work identically across all business channels.

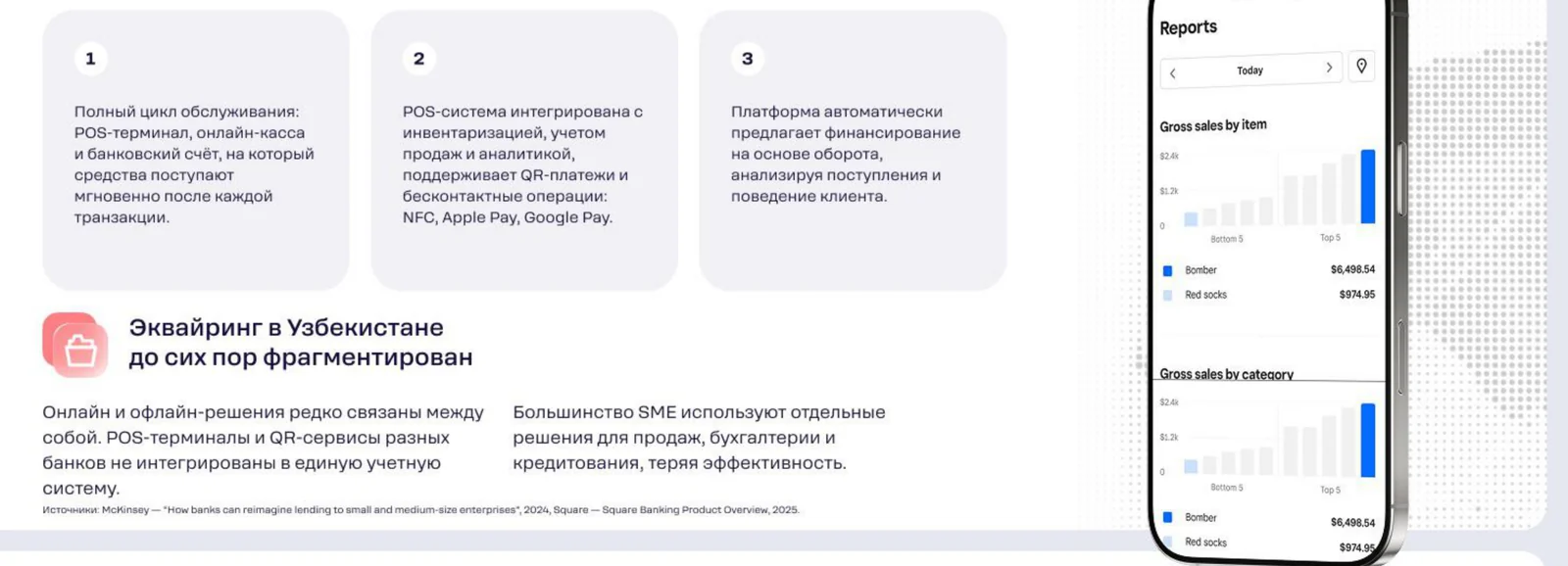

<!-- smeuz-fig:m08_ekvayring_bench start -->

Like the leaders: Square combines the account, acquiring, and sales analytics in a single loop—payment acceptance is built into the business, not relegated to a terminal.

<!-- smeuz-fig:m08_ekvayring_bench end -->Why This Matters for the Bank

Simple onboarding and support for modern scenarios directly affect the turnover passing through the bank. The more business models acquiring is embedded into—from retail to subscription services—the higher the commission revenue and client "stickiness": abandoning the infrastructure that holds up sales is much harder than changing a tariff.

FAQ

What are recurring payments?

Regular automatic subscription charges—for example, a monthly service fee—without the client needing to re-enter card details.

Why does acquiring need APIs and SDKs?

They allow embedding payment acceptance directly into a business's website, app, or checkout, and support complex scenarios like subscriptions and installment payments.

What do digital cards with category limits provide?

A company issues cards to employees with restrictions on amounts and types of spending, controlling expenses without manual receipt reconciliation.

Why is online acquiring onboarding so important?

It removes the main barrier to entry: a business starts accepting payments quickly and transparently, instead of going through a long offline quest with unclear fees.

What does "invisible" acquiring mean for the buyer?

It is a payment that does not distract: the client pays on the website, via QR, or at the checkout equally smoothly and does not think about which bank is behind the transaction.