For small and medium-sized businesses, a bank has long ceased to be just a place to store money. A company expects it to act as a partner that adapts to its structure, rather than forcing it into the rigid frameworks of legacy processes. A study on the digital maturity of SME banking in Uzbekistan shows that it is precisely in customer service where most players have the most noticeable and yet most underestimated reserve.

📄 Download the full research (PDF) — data on 20 Uzbekistan banks and 110 parameters, maturity rating, and methodology.

The Short Answer

Customer service in SME banking is about how much a bank simplifies a business's daily routine: fast onboarding, transparent tariffs, personalized support, and managing multiple legal entities from a single dashboard. The market lacks flexibility and personalization, while the leaders are already shifting to a "partner bank" model. Mature service reduces churn and turns the app into the company's financial control center.

Why "Just an Account" No Longer Sells

A retail customer is retained by convenience and emotion; a corporate customer by time savings and predictability. A business opens an account not for the sake of the account itself, but to pay, hire employees, and grow faster. Once everyone has the basic features, competition shifts from tariff rates to service quality: whoever onboards a company faster, explains the cost of service more transparently, and gathers all of an owner's legal entities in one window is the one who retains the client.

It is also important that the decision to switch banks in B2B is made rationally and collectively: the financial director compares the actual experience of working with the dashboard, not the advertising. Therefore, every extra step in service is not just an annoyance, but a measurable reason to leave for someone who is "clearer and faster."

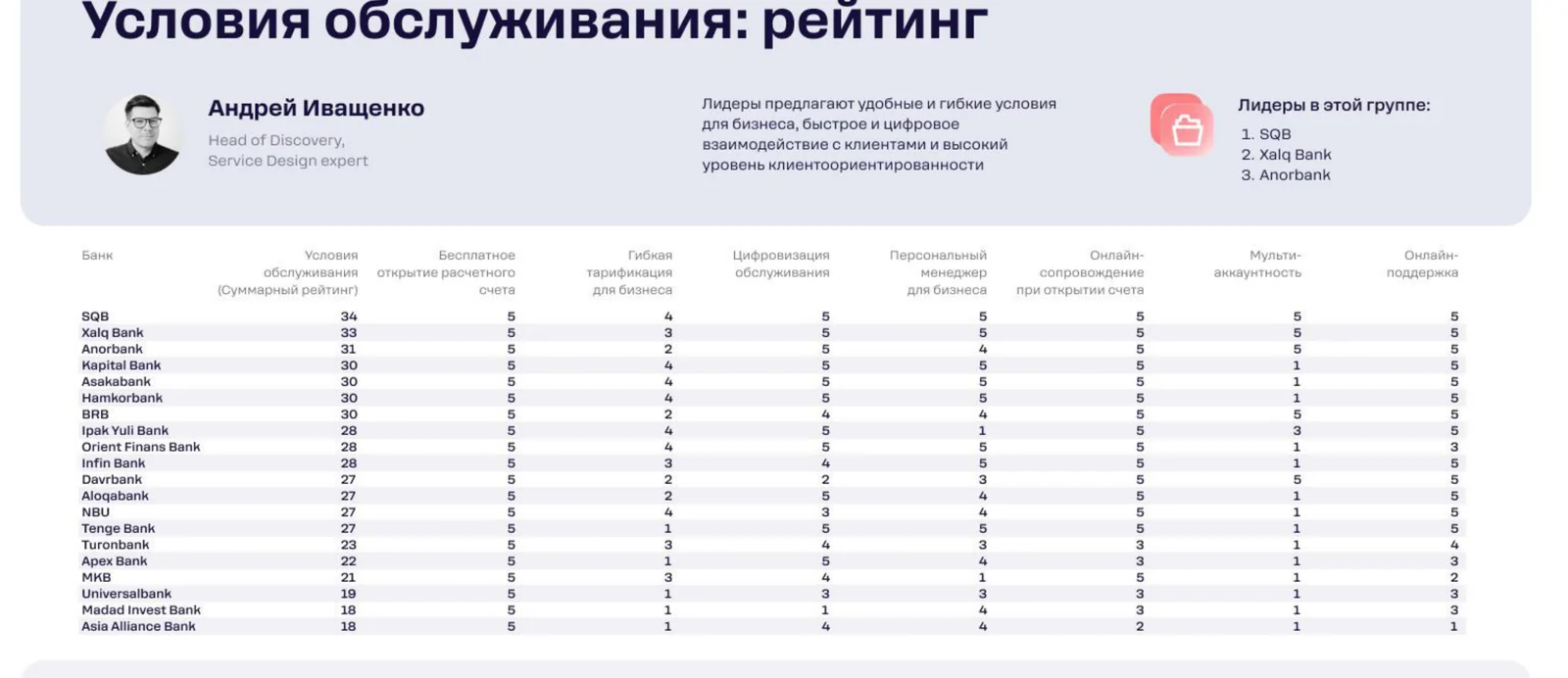

What the Research Showed

Category leaders according to the Rocket Tech research ("Terms of Service"): 1. SQB, 2. Xalq Bank, 3. Anorbank.

<!-- smeuz-fig:m03_servis_rating start -->

Rating by terms of service: transparent tariffs, a personal manager, and working with multiple legal entities are the strong points of the leaders.

<!-- smeuz-fig:m03_servis_rating end -->An analysis of the apps revealed three systemic areas for growth.

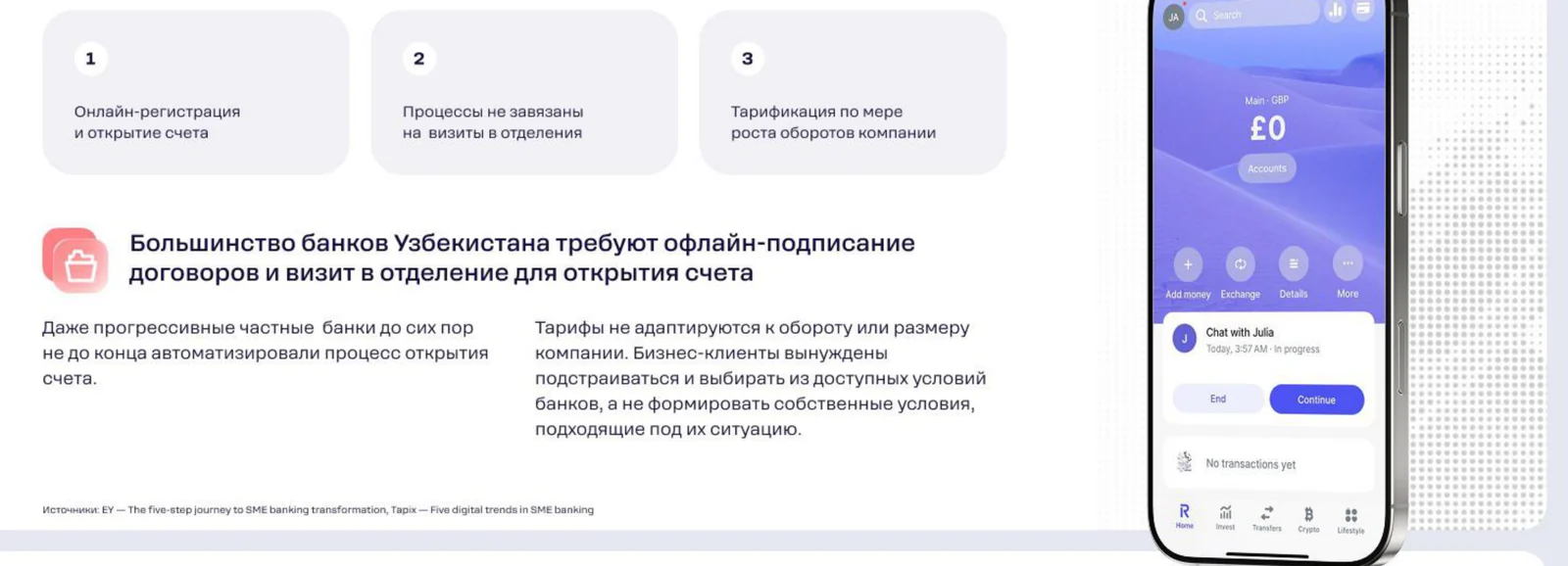

Onboarding and Tariffs

The market suffers from opaque tariffs, and full digitalization at the onboarding stage is still in short supply. It is difficult for companies to understand the final cost of service in advance, and the account opening process itself often requires branch visits and paperwork. There is a lack of flexible tariffs that would cater to different business segments—from micro-entrepreneurs to medium-sized enterprises.

Personal Approach

Dedicated personal managers and a "tailored to the client" support model remain a rarity. Meanwhile, it is precisely the feeling that a real person and a clear channel for resolving issues are assigned to the company that builds long-term trust in the bank.

Multi-Accounting

Managing the accounts of multiple companies, branches, and currencies from a single dashboard is mostly found among the leaders. An owner managing several legal entities has to keep separate logins and switch between them—this is a direct loss of time.

What It Looks Like in Practice

Imagine an owner who has two companies and a sole proprietorship. In an immature bank, this means three separate logins, three sets of bank details, and constant switching just to get an overall picture of the money. Opening an account for a new legal entity again requires a branch visit and a package of documents, and when asked about fees, the manager replies, "it depends on the transactions." In a mature scenario, the same owner sees all three businesses in one dashboard, opens a new account online via eKYC in a matter of minutes, and understands the cost of service in advance through a transparent tariff. The difference is not in a single feature, but in how much time and nerves are spent on routine tasks.

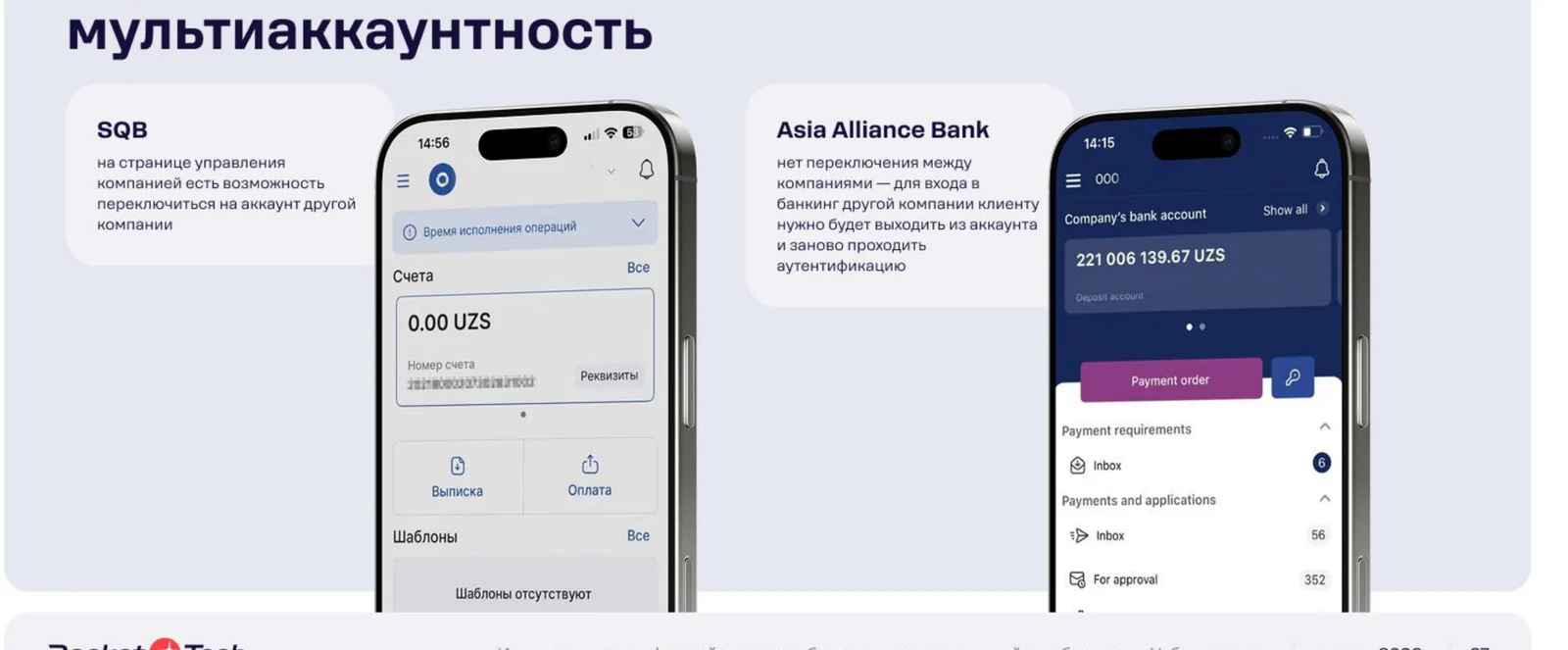

<!-- smeuz-fig:m03_servis_screens start -->

SQB allows managing accounts of multiple companies from a single dashboard. In Asia Alliance, you cannot switch to another company—you have to log out and log in again.

<!-- smeuz-fig:m03_servis_screens end -->How It Is Solved

The gap between the leaders and the rest is closed not by cosmetic changes, but by rebuilding the customer journey:

- Custom tariff packages, where the client controls the cost based on their transaction profile, rather than choosing from rigid "boxes."

- A Relationship Banking model focused on retention and support, rather than a one-time product sale.

- A unified dashboard for managing legal entities, branches, and currencies, and eKYC for fully automated onboarding without visiting a branch.

It is exactly at this level—designing onboarding and personal dashboard scenarios that save the client's time—that the Rocket Tech team operates: auditing the user journey and providing product design for banking apps, where service becomes a reason to stay, not an excuse to leave.

<!-- smeuz-fig:m03_servis_bench start -->

Like the leaders: Revolut Business opens an account entirely online, without a branch visit, and tailors the tariff to the company's turnover.

<!-- smeuz-fig:m03_servis_bench end -->Why This Matters for the Bank

Complex onboarding and opaque tariffs mean expensive support, slow connection of new companies, and easy churn to a competitor. Conversely, a bank that supports a client like a partner gains a higher LTV and a natural platform for cross-selling loans, acquiring, and other services. In the SME segment, where everyone's products are similar, it is the quality of service that turns into a sustainable competitive advantage.

FAQ

What is customer service in SME banking?

It is everything surrounding the account: the speed and transparency of onboarding, tariff flexibility, personalized support, and the ability to manage multiple legal entities from a single dashboard. In B2B, it is measured by the client's saved time, not just the politeness of the support team.

What is relationship banking?

A model in which the bank builds long-term relationships with a business and earns from retention and support, rather than one-off transactions. A clear channel and a "growth partnership" logic are assigned to the client.

Why does a business need a unified dashboard for multiple companies?

Owners often manage several legal entities and branches; switching between separate logins wastes time and increases the risk of errors. A unified dashboard with multi-accounting removes this friction.

What is eKYC?

It is remote customer identification that allows opening an account and passing verification entirely online, without a branch visit or a paper document package.

How do you know if a bank's service is costing a business money?

Look at the time and number of steps required for typical tasks: opening an account, adding an employee, getting a support response, or consolidating turnover across multiple legal entities. If it is slow and opaque, the client is paying the costs with their time.