Speed of access to capital is one of the main needs of a business, but lending processes in many banks remain sluggish and require in-person visits. While competitors spend weeks thinking, the window of opportunity closes. A study on the digital maturity of SME banking in Uzbekistan shows how the market can shift the paradigm—from a paper application to money in an hour.

📄 Download the full research (PDF) — data on 20 banks in Uzbekistan and 110 parameters, maturity rating, and methodology.

The Short Answer

Corporate lending matures when the entire cycle—from application to repayment schedule—takes place online, scoring is automated, and products take the industry into account. Currently, branch visits and standard products without industry specifics prevail. Maturity here is liquidity that the bank offers to a business exactly when it is needed for growth.

Why Speed is Decisive

A cash gap or a lucrative deal will not wait weeks for approval. For a business, the value of a loan heavily depends on how quickly it is available: money "in an hour" and "in two weeks" are fundamentally different products. Therefore, lending is evolving from a "product you go to a branch for" to a "built-in feature that proactively offers money on time."

At the same time, speed should not mean blind risk: it is achieved by automating the assessment, not by abandoning it. Well-built digital scoring accelerates the decision while simultaneously making it more justified.

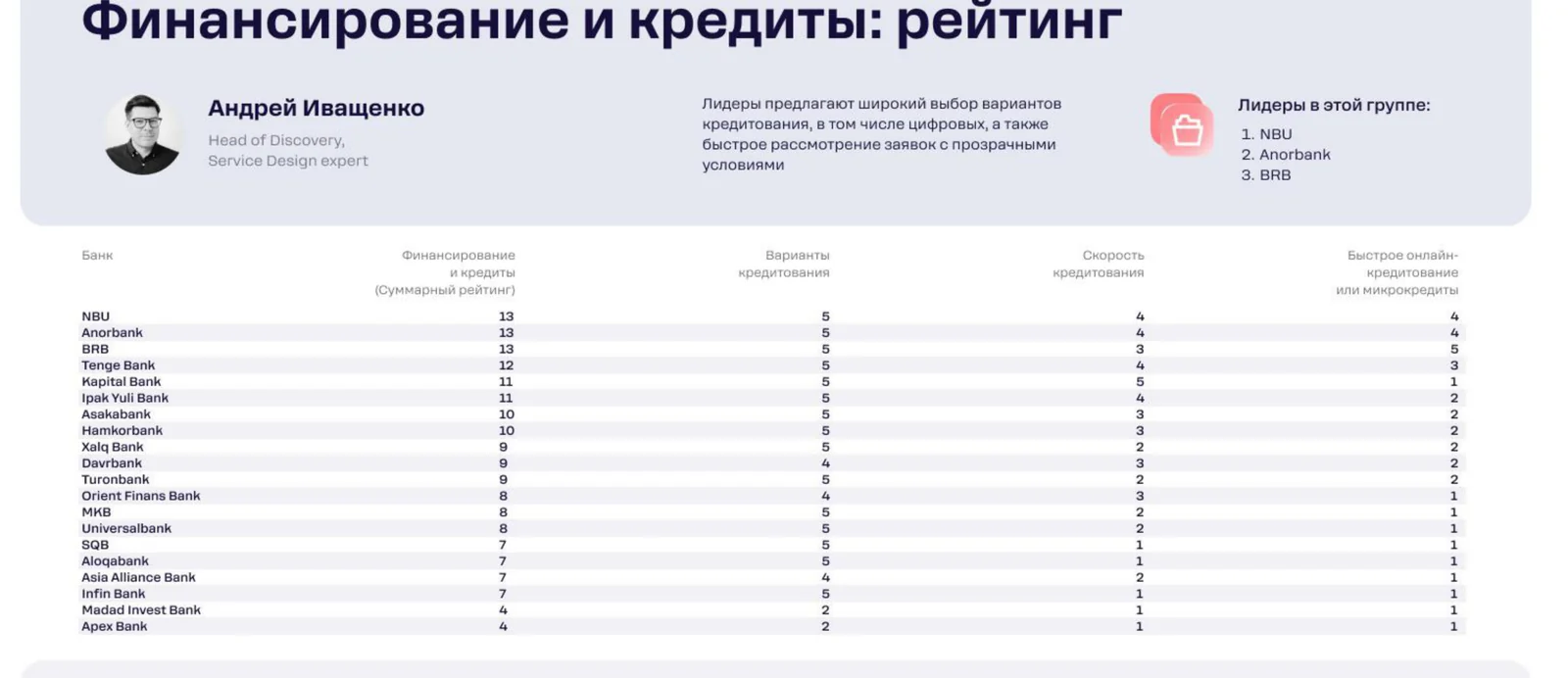

What the Research Showed

Category leaders according to Rocket Tech research ("Financing and Loans"): 1. NBU, 2. Anorbank, 3. BRB.

<!-- smeuz-fig:m10_kredit_rating start -->

Financing and loans rating: fully online cycles and industry-specific products belong to the leaders.

<!-- smeuz-fig:m10_kredit_rating end -->Market growth points add up to a common problem: a loan remains a "heavy" product.

Sluggish Processes

Processing often requires in-person branch visits and paper document flow. For an active business, this is a barrier that cuts off a portion of demand even before an application is submitted.

Lack of Industry Specifics

Standard loan products do not account for business specifics: an exporter, a trading company, and an IT startup have different seasonality and different cash flow logic.

Few Digital Channels

Fully online channels, even for small amounts and microloans, are almost non-existent, although this is exactly where speed matters most.

How It Looks in Practice

A trading company receives a lucrative offer from a supplier—but the purchase must be paid for within a couple of days. In an immature bank, the owner gathers a package of documents, goes to the branch, waits a week for a decision—and the deal falls through. In a mature scenario, they apply directly in the app, automated scoring evaluates them based on transaction history, and the approved limit appears on the same day. Moreover, a bank that sees the client's turnover can offer a loan in advance—before a gap occurs. A loan ceases to be a separate quest and becomes part of an everyday service.

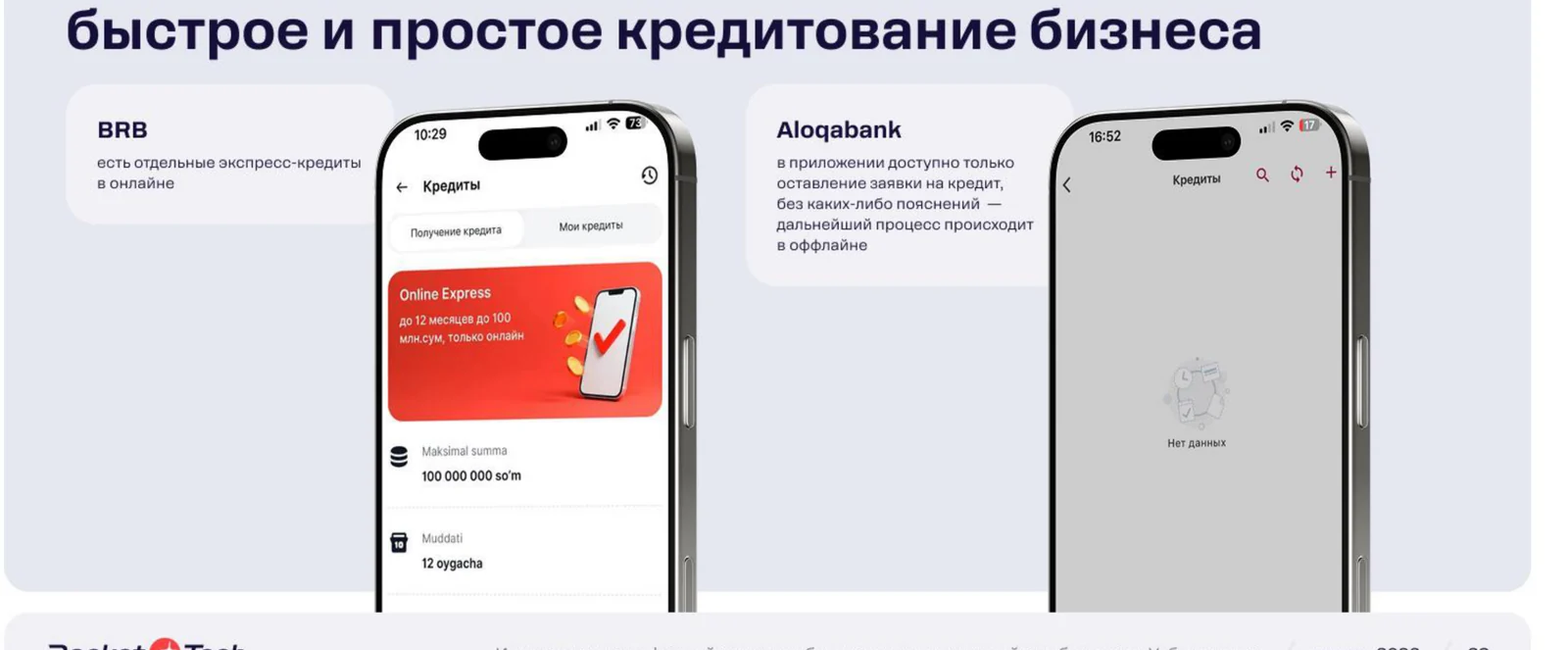

<!-- smeuz-fig:m10_kredit_screens start -->

BRB allows applying for an express loan online. At Aloqabank, lending is still offline—the application goes to the branch.

<!-- smeuz-fig:m10_kredit_screens end -->How It Is Solved

- Niche loan products — for exporters, startups, IT — with seasonal limits tailored to the real business cycle.

- Scoring automation and a full online cycle: from submitting an application to managing the repayment schedule without visiting a branch.

- Predictive analytics for personalized offers based on the client's transaction history — the bank offers a limit before the client even asks for it.

Building such processes—digital scoring, an online application journey, data analytics—is Rocket Tech's profile as a technology partner: we help banks automate the credit pipeline so that a decision takes minutes, not days, without losing control over risk.

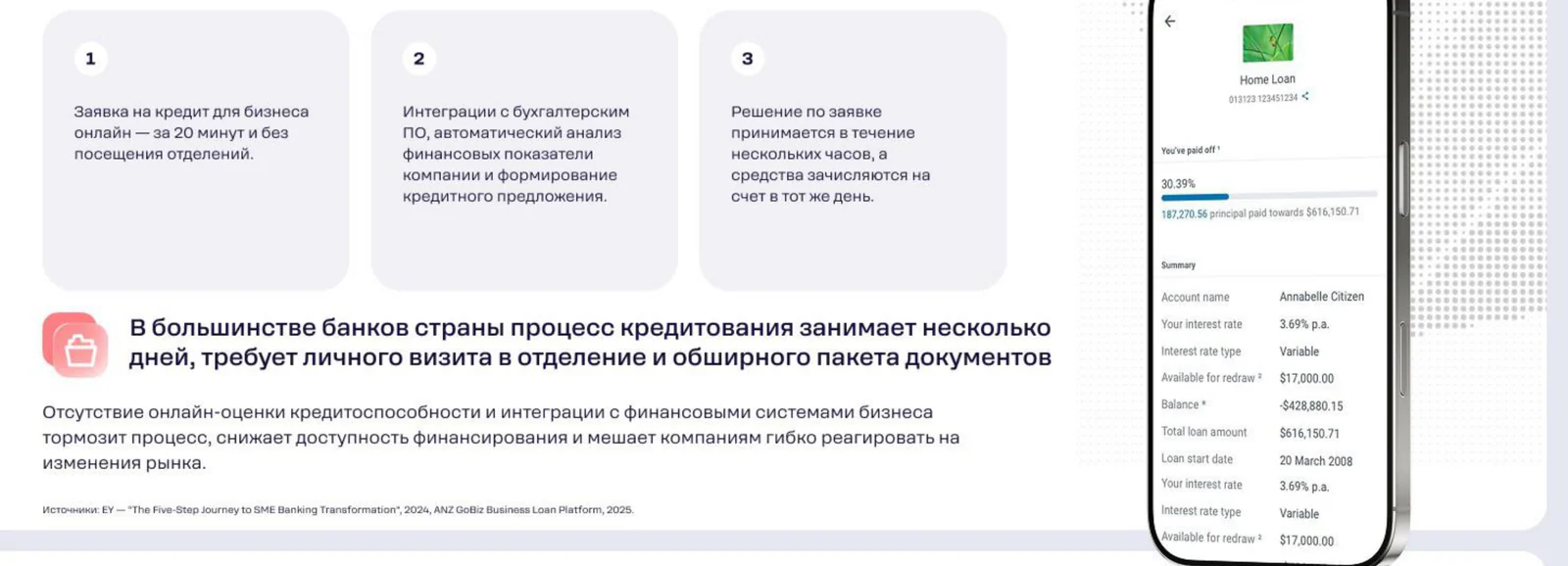

<!-- smeuz-fig:m10_kredit_bench start -->

Like the leaders: ANZ GoBiz issues a business loan decision in 20 minutes online, without a branch visit.

<!-- smeuz-fig:m10_kredit_bench end -->Why This Matters for the Bank

Fast online lending expands the funnel and allows issuing loans where previously the client would leave due to lengthy approvals. Data-driven scoring reduces risks and application processing costs, while personalized offers at the right moment increase conversion into issuance and loyalty. A loan ceases to be a one-time event and becomes a continuous growth service.

FAQ

What is credit scoring?

An automated assessment of a borrower's solvency based on data (including transactional data), which allows making a decision without manually reviewing each application—faster and on a more objective basis.

What does a "full online cycle" of lending mean?

The entire journey—application submission, decision, signing, and managing the repayment schedule—takes place in the app without branch visits or paperwork.

Why are niche loan products needed?

An exporter, a trading company, and a startup have different seasonality and needs; industry-specific products fit the business more accurately and reduce the risk of non-repayment for the bank.

How can a bank offer a loan "in advance"?

Based on the client's transaction history, predictive analytics assesses the need for liquidity and generates a personalized offer—even before the business faces a cash gap.

Does speed increase credit risk?

No, if speed is achieved by automating the assessment rather than abandoning it: digital data-driven scoring is often more accurate than manual review and, at the same time, faster.