The more complex a business structure, the more fine-tuned access settings it expects from its banking dashboard. A growing company outgrows the basic "view/edit" matrix—it needs a model that reflects the real distribution of roles and responsibilities. A study on the digital maturity of SME banking in Uzbekistan shows where the market lags in access architecture.

📄 Download the full research (PDF) — data on 20 banks in Uzbekistan and 110 parameters, maturity rating, and methodology.

The Short Answer

Mature access management means flexible roles for accountants and executives, collaborative work on payments with multi-level approvals, and a full audit trail of actions. Currently, collaborative features are mostly implemented by market leaders, preset role scenarios are missing, and transaction history is minimal. The more complex a client's business, the more important fine-tuning rights and limits becomes for them.

Why the Basic Role Matrix Breaks Down

In a three-person company, a couple of access levels are enough. But as soon as accounting, financial control, and multiple signatories appear, a simple "view/edit" setup stops reflecting the processes: someone needs to prepare a payment, someone needs to approve it, and someone only needs to see reports. Without flexible roles, a business faces a bad choice: either hand out excessive rights and risk security, or bottleneck everything through one person and slow down operations.

As the company grows, this conflict only intensifies—and a bank that doesn't provide fine-tuning starts hindering the business.

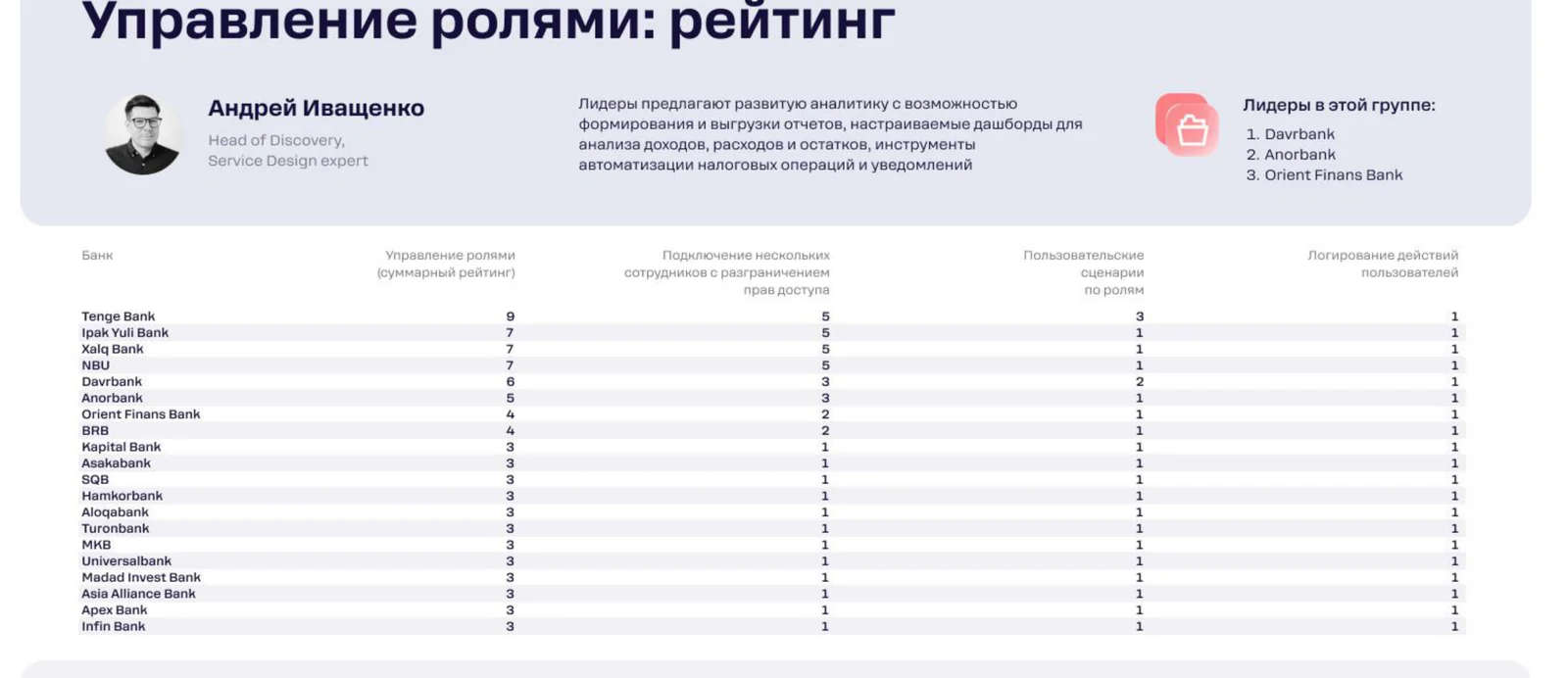

What the Research Showed

Category leaders according to Rocket Tech research ("Role Management"): 1. Tenge Bank, 2. Ipak Yuli Bank, 3. Xalq Bank.

<!-- smeuz-fig:m01_roli_rating start -->

Bank rating by role management: for most, access is designed for a single user; collaborative work and auditing are mainly found among the leaders.

<!-- smeuz-fig:m01_roli_rating end -->Market growth points show that access is designed for a single person.

Collaborative Work

Support for simultaneous work by multiple employees is implemented mainly by the leaders of the table.

No Preset Roles

There is a lack of preset scenarios for typical roles—accountant, executive—which complicates and slows down employee onboarding.

Weak Auditing

Activity tracking mechanisms and transaction history are minimal, and without them, it is difficult to ensure transparency and investigate incidents.

How It Looks in Practice

A company's team is growing: an accountant, a financial director, and an owner appear, each with their own area of responsibility. In an immature bank, access is essentially one-size-fits-all: for the accountant to prepare payments, they are given full rights—and now they can also send them without oversight. The owner either accepts the risk or signs everything themselves, becoming a bottleneck. In a mature scenario, everyone has their own role: the accountant prepares the payment, the financial director approves it, the owner views reports, and the audit system records who did what. A new employee receives the necessary set of rights in one click using a preset scenario. Security and speed no longer conflict.

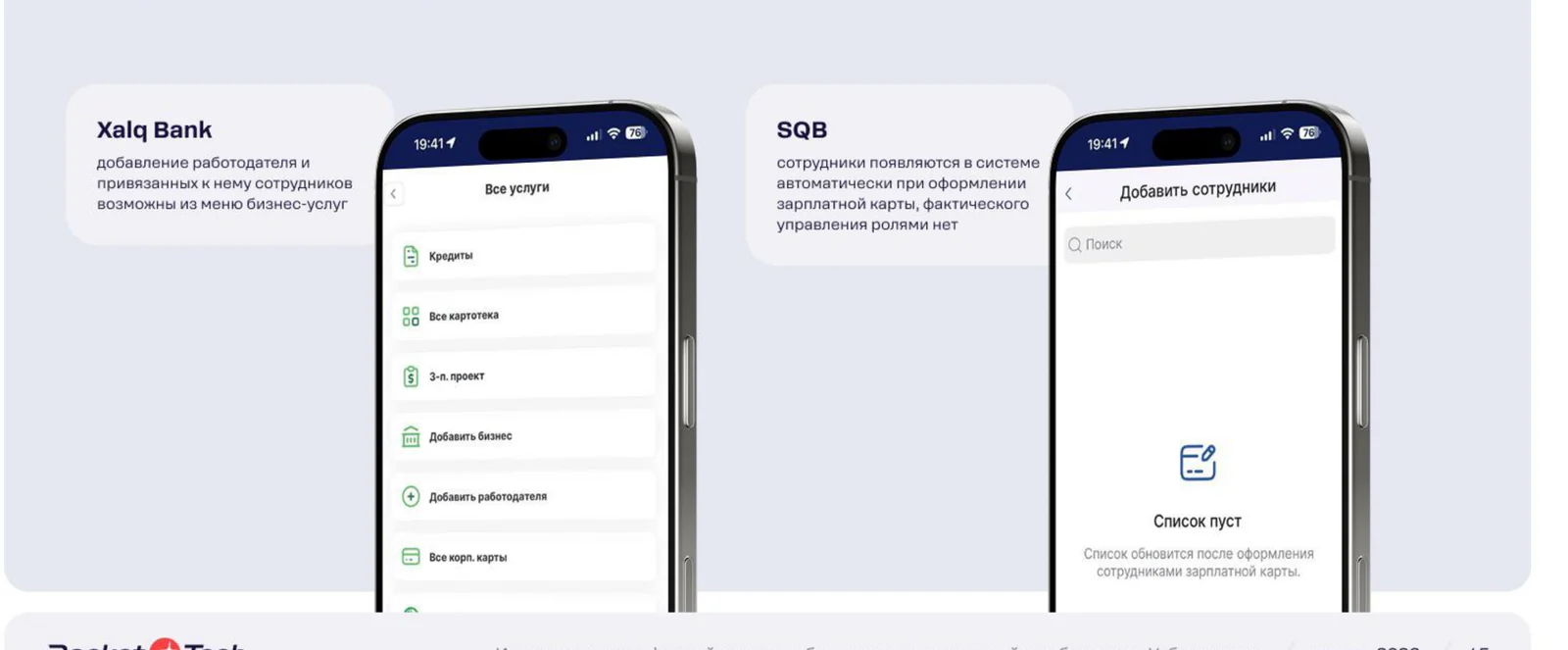

<!-- smeuz-fig:m01_roli_screens start -->

Xalq Bank allows adding an employer and employees from the business services menu. At SQB, employees only appear when issuing a payroll card—there is no separate role management.

<!-- smeuz-fig:m01_roli_screens end -->How It Is Solved

- Full collaborative access with segregation of rights and multi-level payment approvals.

- Preset role scenarios for fast onboarding of new employees without manually configuring every permission.

- Advanced auditing — logging and monitoring actions for transparency and control.

Designing role models that are both secure and user-friendly is the intersection of access architecture and UX where Rocket Tech operates: we help banks implement collaborative access and auditing so that permissions are flexible, payment approvals are reliable, and employee onboarding is fast.

Why This Matters for the Bank

Flexible roles and auditing mean both security and convenience: a business trusts a bank where it can accurately distribute rights and see who did what. For growing companies, this is often a decisive selection criterion: the larger the client, the more important fine-tuned access is to them, and the more costly it is for the bank to lose them due to a primitive role model.

FAQ

What is a role model in a banking dashboard?

A system of permissions where each employee has their own role (prepare a payment, approve, view only) according to their function in the company.

Why is an operations audit needed?

To see who performed an action and when; this increases transparency, simplifies incident investigation, and reduces the risk of abuse.

What does multi-level payment approval provide?

One employee prepares a payment, another approves it—this reduces the risk of errors and fraud in large transactions.

Why do preset role scenarios speed up work?

A new employee gets the appropriate set of rights in one click, without manual configuration of each access level—onboarding takes minutes, not hours.

When is it time for a business to switch to flexible roles?

As soon as more than one person works on finances and a "prepares / approves / controls" division appears—the basic permission matrix is no longer enough.