Closed banking systems force entrepreneurs to multiply manual labor—transferring data from one program to another and increasing the risk of critical errors. Open APIs change this, turning the bank from an isolated system into a business hub. A study on the digital maturity of SME banking in Uzbekistan shows how ready the market is for the Open Banking era.

📄 Download the full study (PDF) — data on 20 banks in Uzbekistan and 110 parameters, maturity rating, and methodology.

The Short Answer

Open APIs are an opportunity for a bank to seamlessly exchange data with business systems: accounting, ERP, and tax authorities. So far, only a few support full integration with 1C, SAP, and QuickBooks, and automatic synchronization with reporting is poorly developed. In the run-up to Open Banking, closed systems lose to those offering clients flawless data exchange with third-party services.

Why APIs Are About Saving Labor

Every manual transfer of a statement to accounting is wasted time and a potential error that will later surface in reporting. APIs remove the middleman: data flows automatically between the bank and business systems. For the client, this means less routine and fewer risks; for the bank, it means a place at the very center of the company's digital perimeter.

Openness is also a strategic choice. A bank that shares data via standardized interfaces becomes a platform around which services are built; a closed bank remains just one of many payment providers.

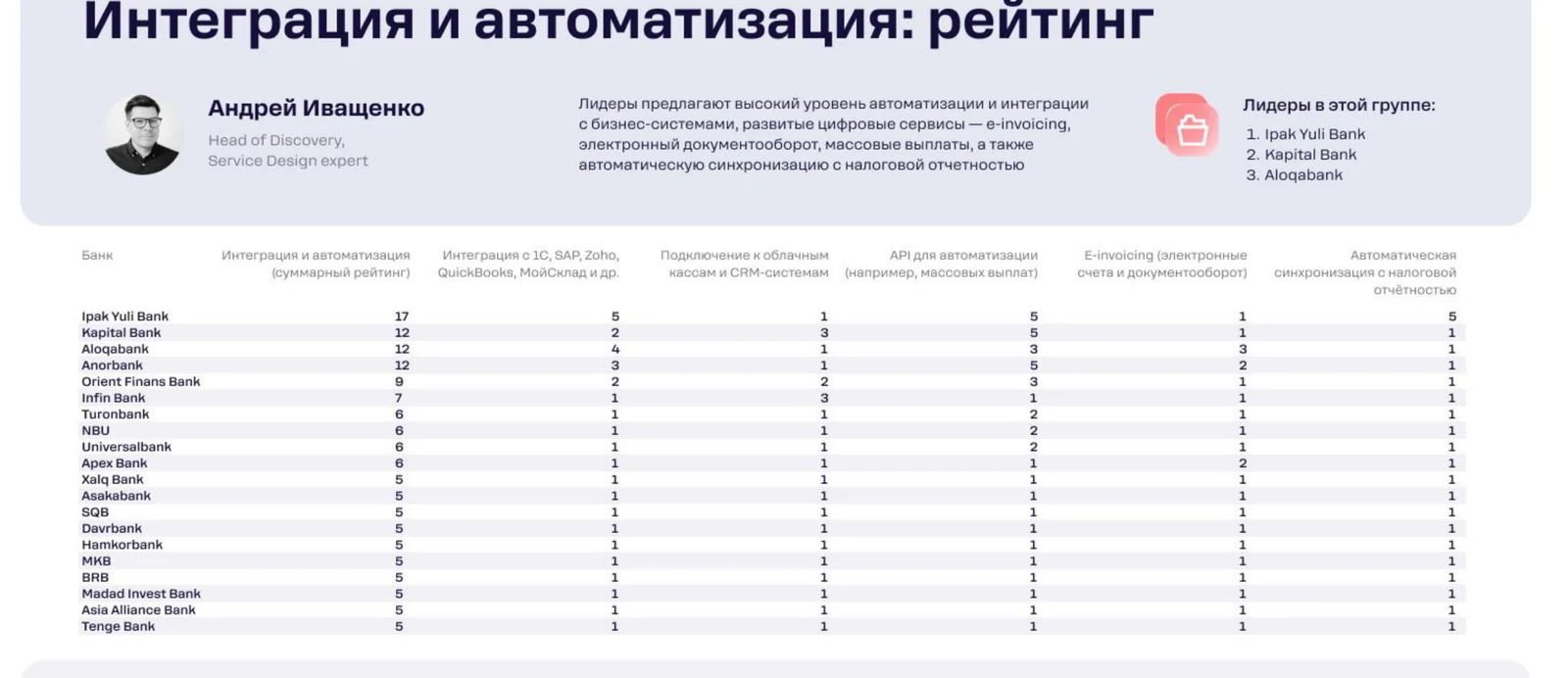

What the Study Showed

Leaders in this area according to the Rocket Tech study ("Integration and Automation"): 1. Ipak Yuli Bank, 2. Kapital Bank, 3. Aloqabank.

<!-- smeuz-fig:m11_api_rating start -->

Integration and automation rating: only a few banks support deep integration with 1C, SAP, and QuickBooks.

<!-- smeuz-fig:m11_api_rating end -->Market growth points show that integration maturity is still low.

Closed Systems

Businesses are forced to manually transfer data between the bank and accounting programs, which is slow and prone to errors.

Few Deep Integrations

Full integration with 1C, SAP, and QuickBooks is supported by only a few players, even though these systems are the working standard for accounting.

Weak Exchange with Reporting

Bulk payouts and automatic synchronization with tax reporting are poorly implemented, leaving businesses with manual reconciliation.

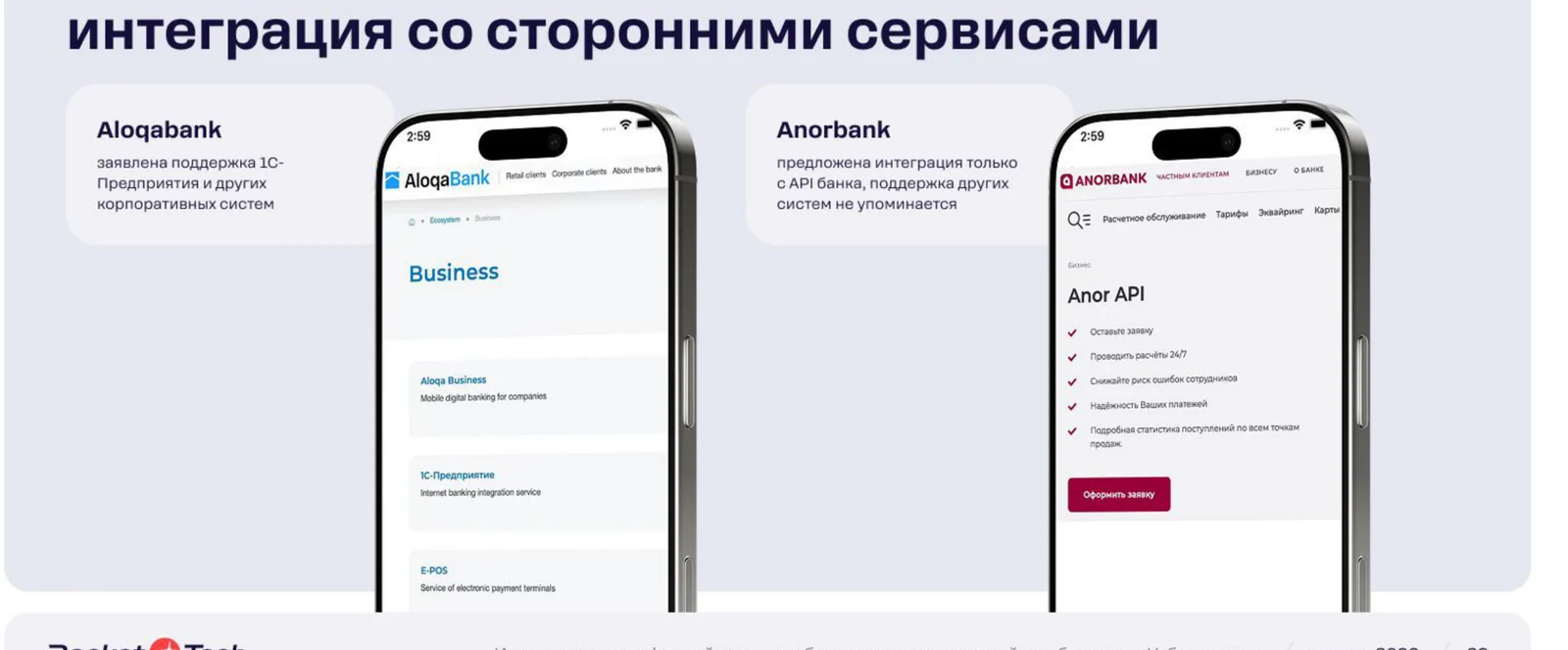

How It Looks in Practice

An accountant is closing the month. In an immature bank, they download the statement, manually transfer transactions to 1C, reconcile them line by line, and separately prepare data for the tax office—a whole day of painstaking work where any typo will surface in the report. In a mature scenario, the bank is connected to the accounting system via a connector: transactions flow into 1C automatically, reconciliation takes minutes, and reporting data goes through an established channel without manual export. The accountant focuses on control, not copying rows—and errors decrease simply because manual transfer disappears.

<!-- smeuz-fig:m11_api_screens start -->

Aloqabank has its own Business-API and 1C support. Anorbank offers integration only through Anor API.

<!-- smeuz-fig:m11_api_screens end -->How It Is Solved

- Connectors to ERP systems and setup of automatic two-way data exchange.

- APIs for bulk payouts and electronic document management.

- Automatic data transmission channels to tax systems for SMEs.

Developing API platforms and connectors, embedding the bank into the client's 1C/ERP/accounting systems—this is what Rocket Tech does as a technology partner: we turn the bank from an isolated system into a hub around which the entire digital perimeter of the business is built.

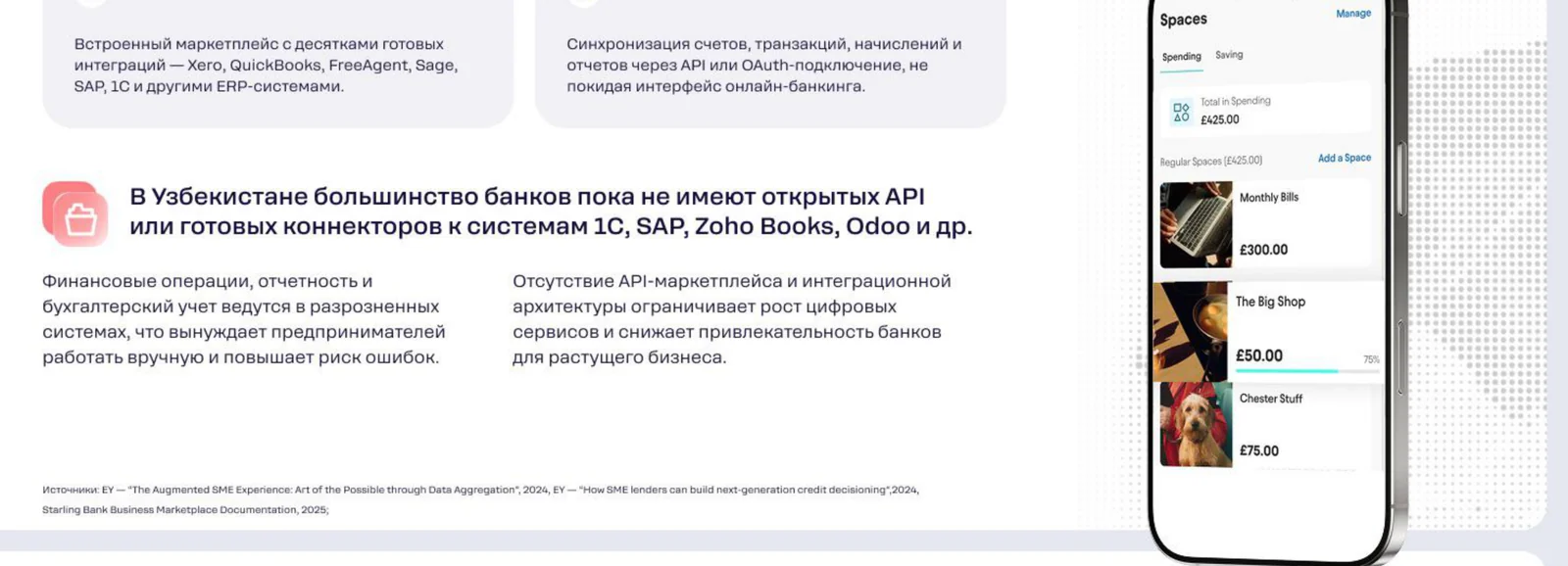

<!-- smeuz-fig:m11_api_bench start -->

Like the leaders: Starling is a marketplace of integrations with Xero, QuickBooks, Sage, and other ERPs right in the online bank.

<!-- smeuz-fig:m11_api_bench end -->Why This Matters for the Bank

A bank with open APIs becomes the integration point for all of the client's business systems—meaning it is much harder to replace. This simultaneously drives retention, reduces operational load, and creates a new layer of services to monetize. In the logic of Open Banking, platforms win, not closed systems, and APIs are the entry ticket to this logic.

FAQ

What is Open Banking?

A model in which a bank provides data and payment functions to trusted third-party services via standardized APIs with the client's consent, creating an ecosystem around the account.

Why integrate a bank with 1C or an ERP?

So that payments, statements, and documents synchronize automatically, without manual transfer and errors, saving the accounting department's time.

What is a connector?

A ready-made module that links the bank with an external system (accounting, ERP) and sets up automatic data exchange between them.

Why is an open bank more advantageous than a closed one?

An open bank becomes a platform around which services are built, retaining the client through integrations; a closed one remains one of many interchangeable payment providers.

Is it safe to share data via API?

Yes, if the exchange occurs via standardized interfaces with the client's consent and access control—this is exactly how the Open Banking model works.