Protecting corporate clients' capital requires a shift from simple passwords to a multi-layered security architecture—one that remains invisible to the user. Security that hinders work is eventually bypassed by employees and ceases to protect. A study on the digital maturity of SME banking in Uzbekistan shows how close the market is to this balance.

📄 Download the full research (PDF) — data on 20 Uzbekistan banks across 110 parameters, maturity ranking, and methodology.

The Short Answer

Mature corporate security means modern multi-factor authentication, deep integration of digital signatures, and role-based automated limits, all remaining invisible in the daily routine. Currently, 2FA is not ubiquitous, digital signatures are sometimes merely formal, and limits require manual intervention. Reliable protection must be practically invisible to the client and absolutely insurmountable to threats.

Why Security Must Be Invisible

If protection creates friction, employees look for workarounds—writing down passwords, sharing access, disabling checks—and it stops working. The goal of a mature architecture is to make security part of the workflow: biometrics instead of passwords, automated limits instead of manual checks, and one-touch transaction confirmation. Then the protection works without creating daily resistance.

For business, it is also a matter of trust: a company entrusts its capital to a bank, and any incident damages not only finances but also relationships.

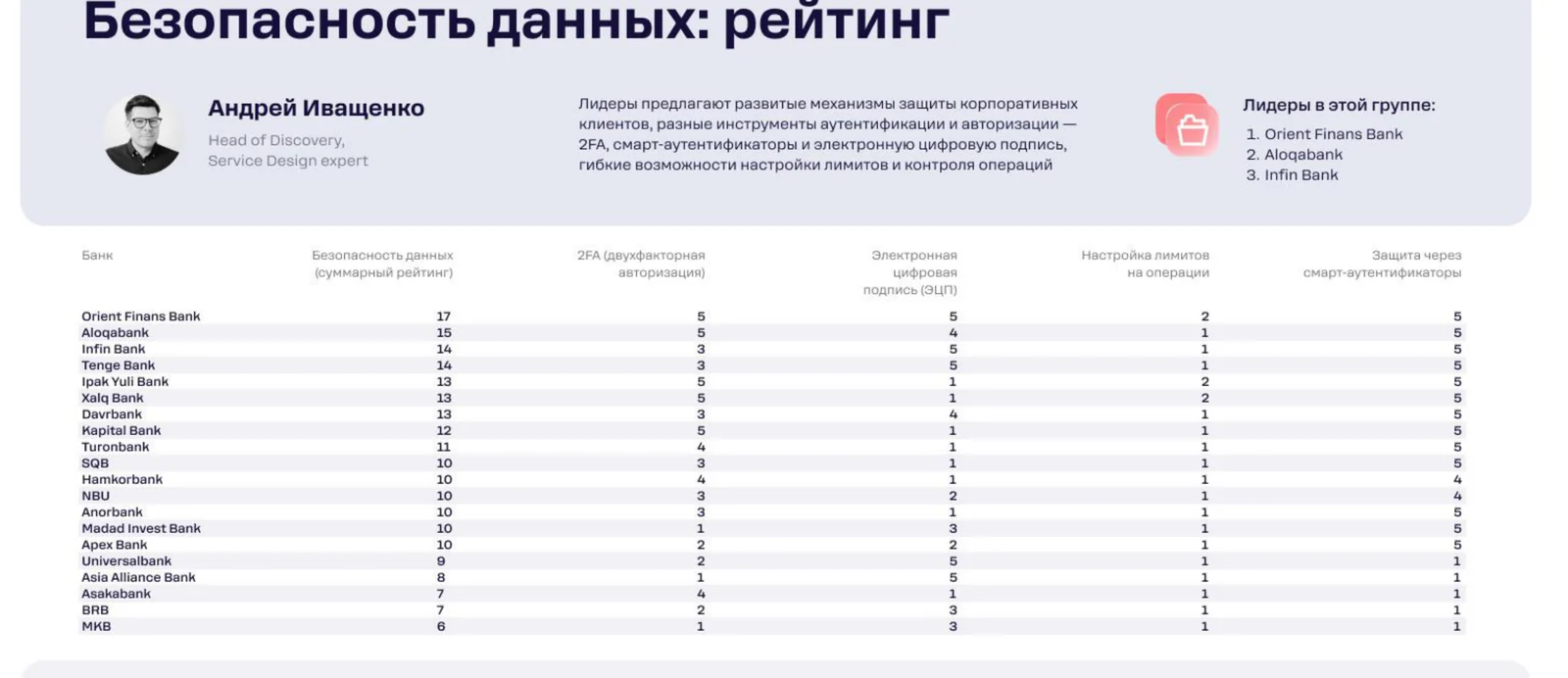

What the Research Showed

Category leaders according to Rocket Tech research ("Data Security"): 1. Orient Finans Bank, 2. Aloqabank, 3. Infin Bank.

<!-- smeuz-fig:m04_security_rating start -->

Data security ranking: modern 2FA, digital signatures, and auto-limits are distributed unevenly across the market.

<!-- smeuz-fig:m04_security_rating end -->Market growth points show that the approach to security is still uneven.

Uneven 2FA

Two-factor authentication is not present everywhere and is often limited to basic methods.

Formal Digital Signatures

Support for electronic digital signatures sometimes remains a mere formality and does not cover key processes.

Manual Limits

Transaction limit control is implemented in a limited way and requires constant manual intervention, which is both inconvenient and risky.

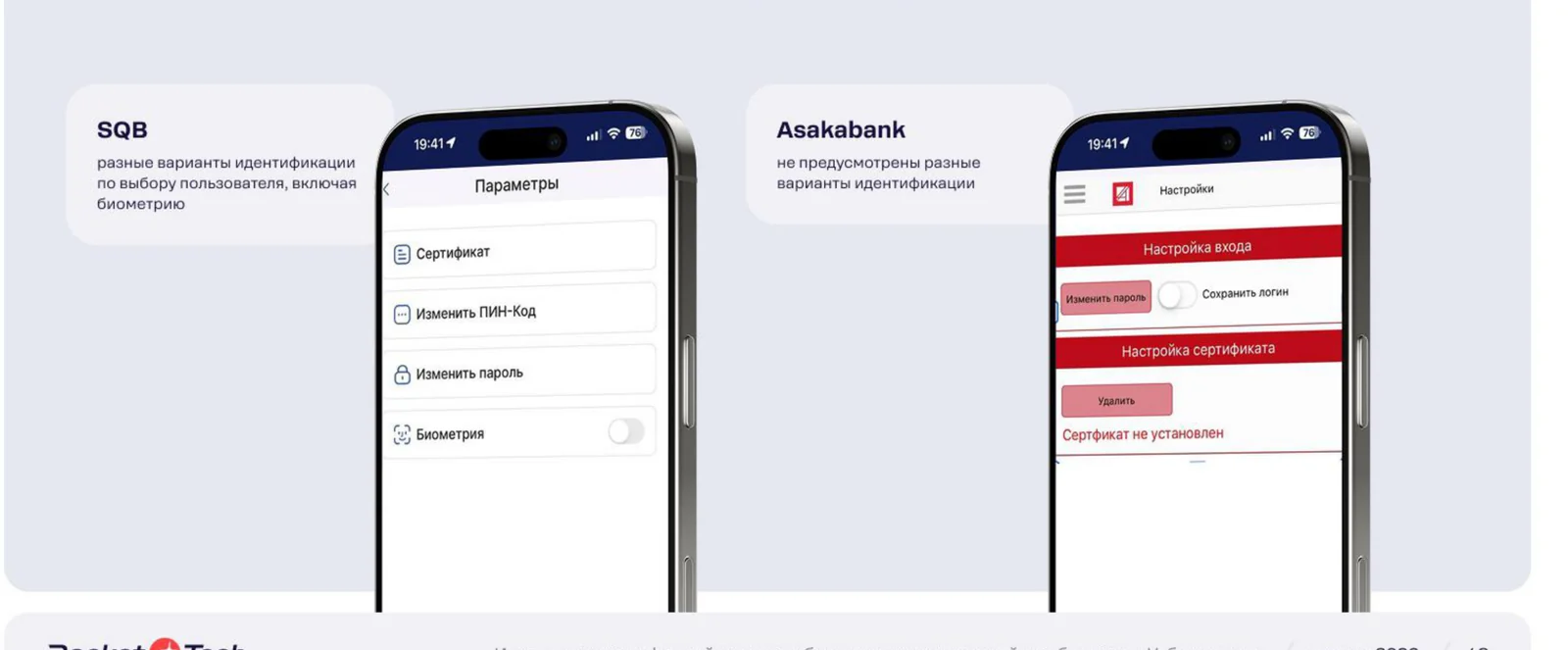

How It Looks in Practice

A CFO goes on a business trip, and the company needs to make an urgent payment. In an immature bank, the signature is "tied" to a branch or a token left in the office, 2FA arrives via an inconvenient channel, and limits can only be changed through a manager—the transaction stalls. In a mature scenario, the director confirms the payment using biometrics on their phone, the digital signature works remotely with legal validity, and limits are already configured by roles and trigger automatically. Security is not weakened in this process—on the contrary, it is more reliable than a password on a piece of paper—but it does not hinder work. This exact balance distinguishes mature protection.

<!-- smeuz-fig:m04_security_screens start -->

SQB offers several methods for login and transaction confirmation. Asakabank has a limited choice of authentication options.

<!-- smeuz-fig:m04_security_screens end -->How It Is Solved

- Modern authorization—biometrics, hardware tokens, and push confirmations instead of vulnerable passwords.

- Deep integration of digital signatures into all key business processes for fully remote work.

- Automated limits with flexible role-based configuration and the implementation of smart authenticators.

Building such "invisible" protection—at the intersection of security and user experience—is part of Rocket Tech's expertise: we help banks implement modern authorization and digital signatures in a way that is convenient for the client's daily work while keeping the system resilient to threats.

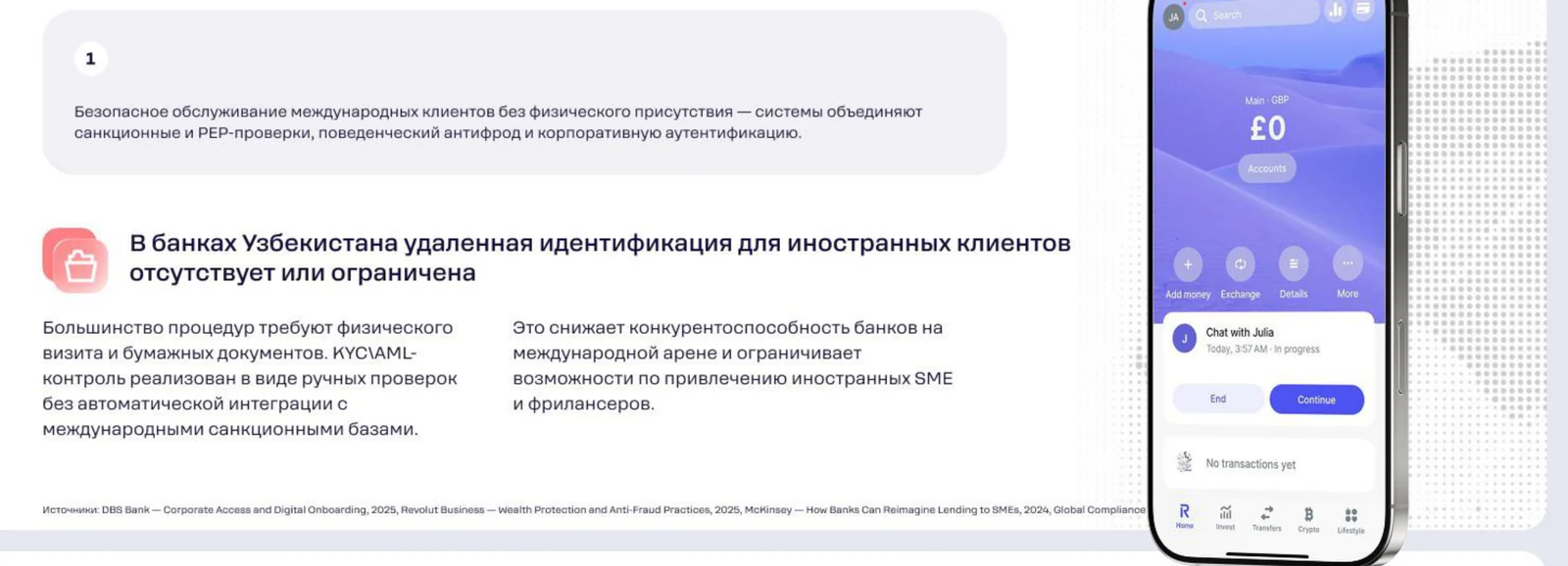

<!-- smeuz-fig:m04_security_bench start -->

Like the leaders: DBS, OCBC, and Revolut remotely identify clients (KYC/AML) and check them against sanction databases without a branch visit.

<!-- smeuz-fig:m04_security_bench end -->Why It Matters for the Bank

For business, security is a matter of trust in the bank as a whole. Incidents cost reputation and money, and inconvenient protection drives clients to competitors just as much as weak protection does. A mature security architecture resolves this conflict: it simultaneously reduces risks and improves the experience, meaning it works for both client retention and the bank's reputation.

FAQ

What is two-factor authentication (2FA)?

Confirming a login or transaction with a second factor besides a password—for example, a code, push notification, or biometrics.

Why are digital signatures needed in corporate banking?

An electronic signature allows for legally binding signing of documents and payments remotely, without paper or branch visits.

What are role-based automated limits?

Restrictions on transaction amounts and types tied to an employee's role and applied automatically, without manual checks every time.

Can security be convenient?

Yes—if it is built into the workflow: biometrics, push confirmations, and automated limits protect without forcing the employee to overcome barriers every time.

What is more dangerous: weak or inconvenient protection?

Both are dangerous: weak protection lets threats through, while inconvenient protection is bypassed by employees and stops working. Therefore, maturity means reliability plus convenience at the same time.