Local context dictates its own rules: digital solutions must work stably not only in metropolises with perfect internet but also in the regions. Ignoring this means cutting off a significant part of the business. A study of SME banking digital maturity in Uzbekistan shows that scaling requires technological empathy for clients' infrastructure constraints.

Download the full study (PDF). Data on 20 banks in Uzbekistan and 110 parameters, maturity rating, and methodology.

The short answer

Regional maturity is when services work stably outside the capital: a modern network of devices, multi-banking tools, and joint products. While many banks are focused on large cities, regions lack new-generation ATMs, and combining cards from different banks is rarely seen. Scaling high-quality SME banking requires deep regional adaptation.

Why regions are not just a "smaller capital"

The context is different in the regions: connectivity can be unstable, the device fleet is older, client habits differ, and the share of cash is higher. A solution designed only for the perfect conditions of a metropolis stalls there — not because the client is "wrong," but because the product did not account for their environment. Technological empathy means considering these constraints within the product itself, rather than putting regions off "for later."

For a bank, this is also a question of growth: competition for the capital client is high, while there is a lack of high-quality digital services in the regions — that is where the untapped demand lies.

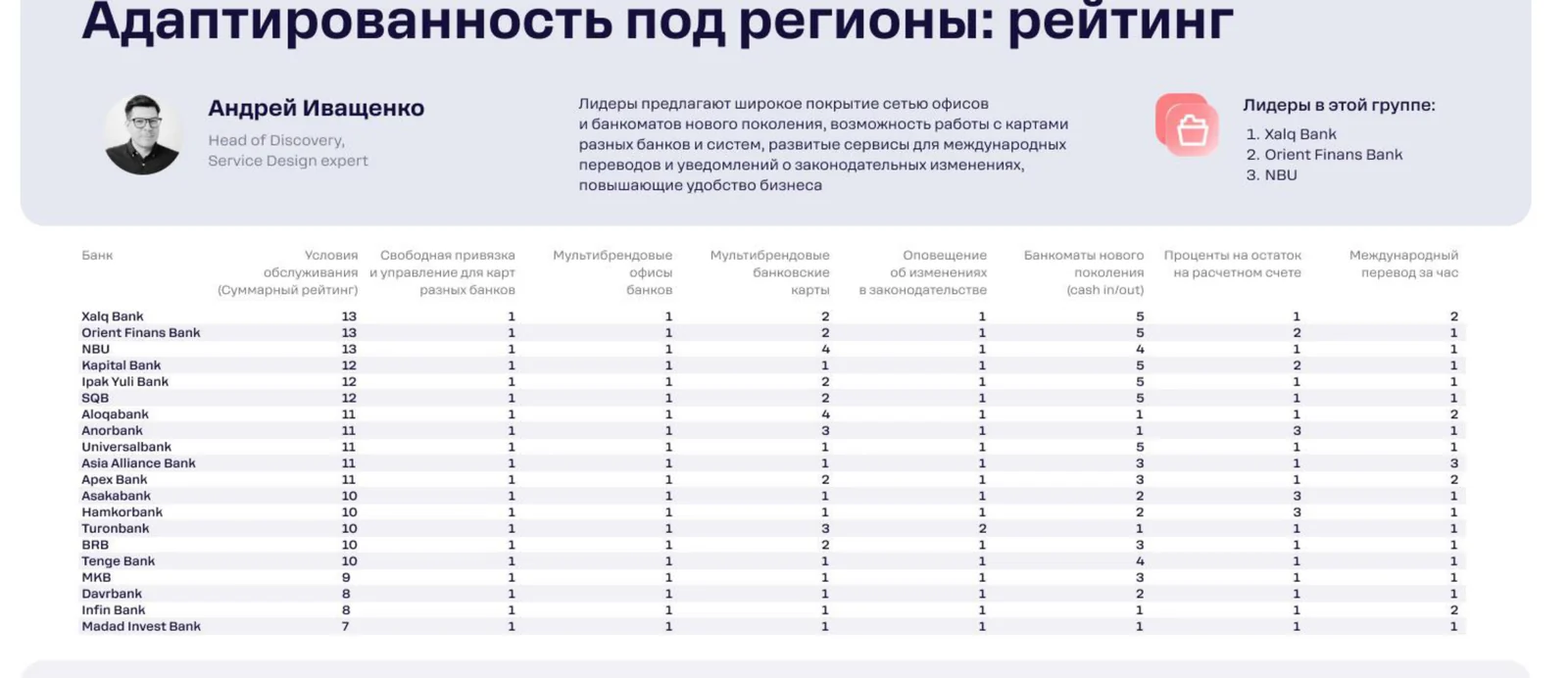

What the study showed

Leaders in this area according to the Rocket Tech study ("Regional Adaptation"): 1. Xalq Bank, 2. Orient Finans Bank, 3. NBU.

Regions are currently served last — this is evident in three things.

Capital focus

Many banks are focused on large cities; regions lack new-generation ATMs with modern scenarios.

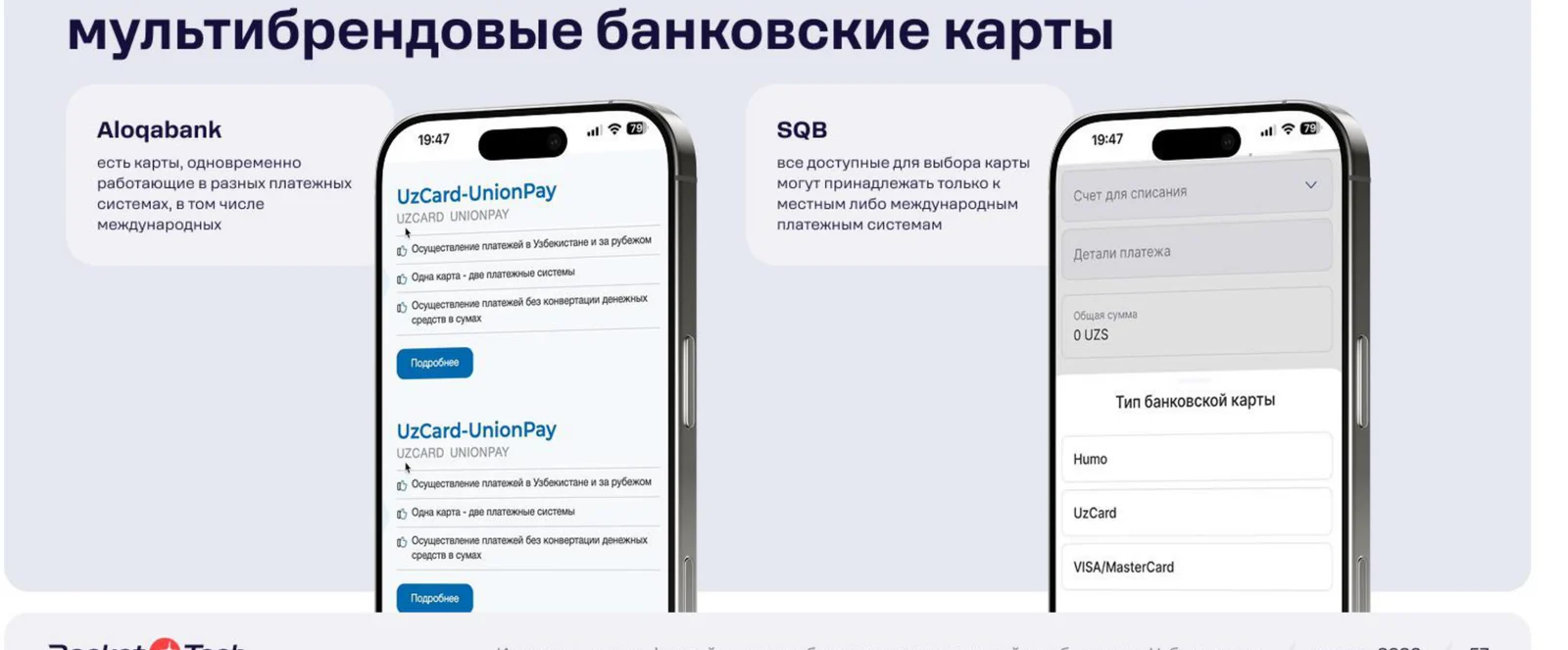

No multi-banking

The function of managing cards from different banks in a single interface is rarely implemented, although it is an obvious convenience for the client.

Rare collaborations

Multi-brand products and joint offices are extremely rare, yet they are exactly what helps close infrastructure gaps faster.

How it looks in practice

A small business operates in a regional center. The internet sometimes drops here, the nearest modern ATM is in another district, and the owner has cards from different banks, each of which has to be checked in a separate app. A service designed only for the stable connectivity of a metropolis regularly fails here. But where the region has been considered, the app works correctly even on an unstable network, there is a smart ATM nearby with cash acceptance and biometrics, and cards from different banks are visible in a single interface. The business receives the same level of service as in the capital — and chooses the bank that took care of this.

How this is solved

- Updating the device network — smart ATMs (cash in/out, biometrics) in the regions, not just in the capital.

- Universal tools for combining cards from different banks in a single interface.

- Bank collaborations for joint products and instant cross-border payments.

Rocket Tech helps banks create services that work equally well in the capital and in the regions: we account for unstable connectivity, an older device fleet, and client habits right in the product.

Why this matters for the bank

Regions mean client base growth where competition is lower. The bank that is the first to make services stable and convenient outside the capital gains a loyal audience and outpaces players with a "capital" focus. In essence, regional adaptation is not an expense to "catch up," but an investment in an untapped market.

FAQ

What are smart ATMs?

New-generation devices with cash acceptance and dispensing (cash in/out) and biometrics, which cover more scenarios without a branch visit.

What is the benefit of combining cards from different banks in a single interface?

The client sees and manages cards from several banks from one app, which is more convenient and increases loyalty specifically to such a bank.

Why is regional adaptation important for fintech?

Because connectivity, devices, and habits in the regions differ; the product must account for these constraints, rather than relying on the perfect conditions of the capital.

Why is it profitable for a bank to go into the regions?

Competition for the capital client is high, while there is little high-quality digital service in the regions — that is where untapped demand and a loyal audience lie.

How to make an app resilient to weak connectivity?

Design it with an unstable network in mind: correct operation of offline scenarios, economical traffic, and resilience to disconnections are part of the product's regional adaptation.