In corporate banking, the interface is not a storefront, but a working tool where company employees spend hours every week. And if in retail a clunky screen costs the bank a client churn, in the B2B segment it costs the client working time, which means direct money. A study of SME banking digital maturity in Uzbekistan shows: this is exactly where most players have their most underestimated reserve.

Download the full research (PDF). Data on 20 Uzbekistan banks and 110 parameters, maturity rating, and methodology.

The Short Answer

UX/UI in business banking directly affects the client's operational costs: the faster and clearer the interface, the less time the accountant and financier spend on routine tasks. The weakest points in the market are the speed of regular operations, mobile versions, and personalization for employee roles. This is not aesthetics, but measurable savings for business.

Why Business Interfaces Follow Different Rules

A retail app is designed for one person and one-off actions: transfer, pay, check balance. A corporate interface is designed for a team and repetitive scenarios: an accountant generates dozens of payment orders, a financial director approves limits, a manager checks balances across multiple accounts. The same operation here is performed not once, but hundreds of times a month—so every extra click and every unclear phrasing multiplies by volume and turns into hours of lost time.

Hence the main principle: in B2B, convenience is measured not by "like / dislike", but by how many steps and seconds it takes to complete a standard task. Good corporate UX is invisible—it simply doesn't get in the way of work.

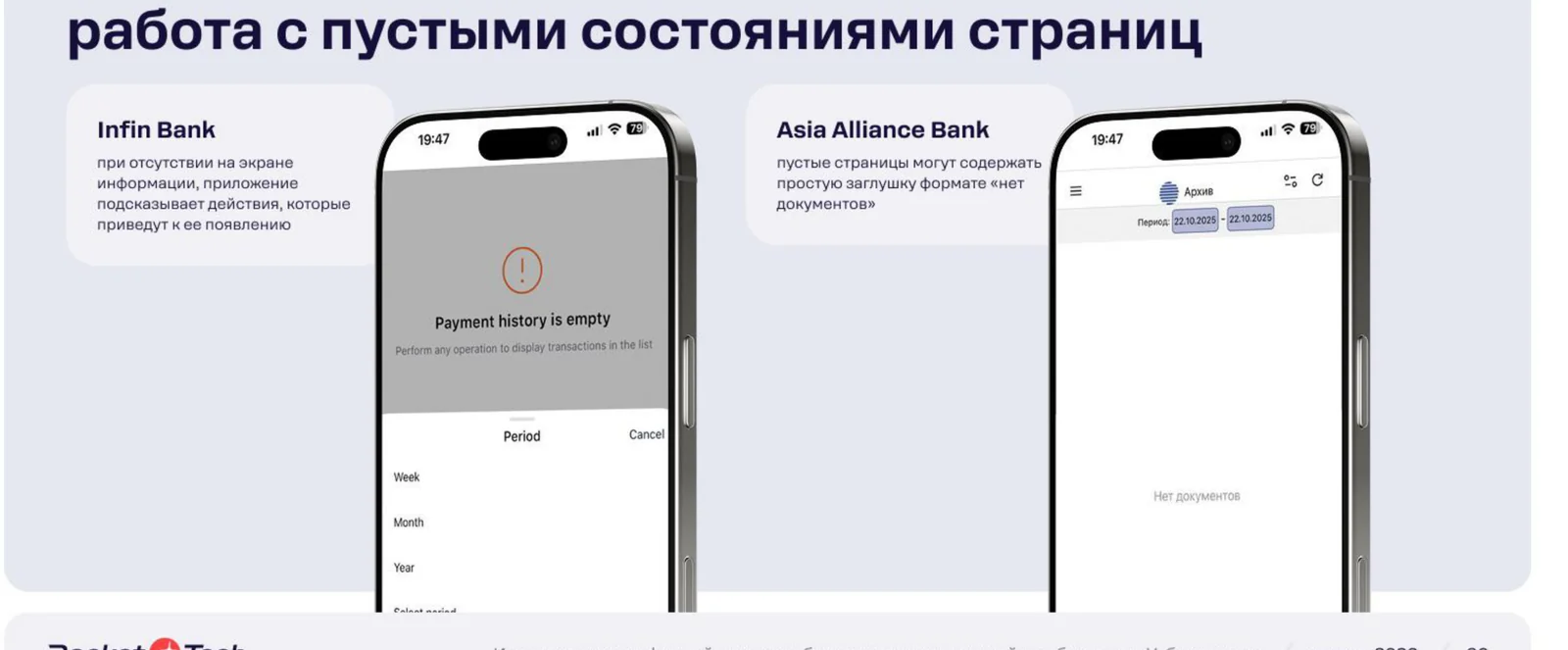

What the Research Showed: Three Growth Areas

Category leaders according to Rocket Tech research ("Informativeness and Convenience"): 1. Anorbank, 2. Infin Bank, 3. Kapital Bank.

Speed of Routine Operations

Most banks noticeably lag behind market leaders in the speed and convenience of performing regular tasks—bulk payments, document exports, repetitive operations. Where leaders allow completing a standard action in two or three taps, for others the same path is stretched across extra screens and confirmations. For the client, this is not an abstraction, but concrete minutes that an employee wastes every day.

Mobile-First and Adaptability

The modern approach, where an app is designed primarily for mobile devices (mobile-first) and correctly adapts to any screen, is far from universally implemented. For a small business owner, this is critical: they manage the company on the go and expect that confirming a payment or checking a balance from a phone is just as convenient as on the web.

Personalization and Roles

Interface settings and adaptation for a specific user are still highly limited. Meanwhile, an accountant, a director, and an owner have different tasks and different access levels—and an interface that shows everyone the same thing forces everyone to wade through unnecessary features.

How It Is Solved: The Approach to Corporate Banking UX

The gap between the leaders and the rest is closed not by cosmetic redesign, but by working with scenarios. In practice, these are three directions:

- Scenario and navigation optimization. First, it is determined which tasks clients perform most often, and then these exact paths are reduced to a minimum of steps. Redesign starts not with a picture, but with a map of real user actions.

- Unified visual language and role-based dashboards. A single style across all sections reduces cognitive load, while individual role-based panels (accountant, director, owner) show everyone only what they need for work.

- Simplified login without compromising security. Biometrics and multi-factor protection remove friction during authorization while maintaining the security level mandatory for corporate data.

Rocket Tech does exactly this: scenario audits, role-based interfaces, and mobile apps for banks and fintech. The goal of such UX is not to "make it pretty," but to reduce the client's time spent on routine and relieve the bank's support team.

Why This Matters for the Bank

A poor interface means more than just dissatisfied users. It means more expensive support (clients call and write about every unclear step), slow onboarding of new companies, and churn to whoever is "simply more convenient." In the SME segment, where the client chooses a bank rationally and easily compares products, mature UX turns into a direct competitive argument, not just a nice addition.

FAQ

What is UX/UI in the context of business banking?

It is how the corporate banking app interface is structured and how quickly and clearly company employees perform work tasks in it—from bulk payments to limit approvals. In B2B, convenience is measured in saved working time, not just appearance.

Why is mobile-first important for business apps?

A small business owner manages the company on the go and expects key operations—payment confirmation, balance checks—to be as conveniently accessible from a phone as on the web. If the mobile version is stripped down or inconvenient, the bank loses standing in the client's eyes even with a strong web platform.

How do you know if a bank's interface is costing a business money?

The indicators are the number of steps for a standard operation, the time spent on a bulk payment, the frequency of support requests regarding "unclear" screens, and the onboarding speed of new employees. If a routine task requires extra clicks, the client pays for these costs with their working time.