Key takeaway

Users need more than just pretty pie charts; they need real insights and advice based on their data. A financial tracking tool will only be successful when it works 100% autonomously, accurately recognizing even non-standard transactions, and communicates with the client in clear, non-patronizing language.

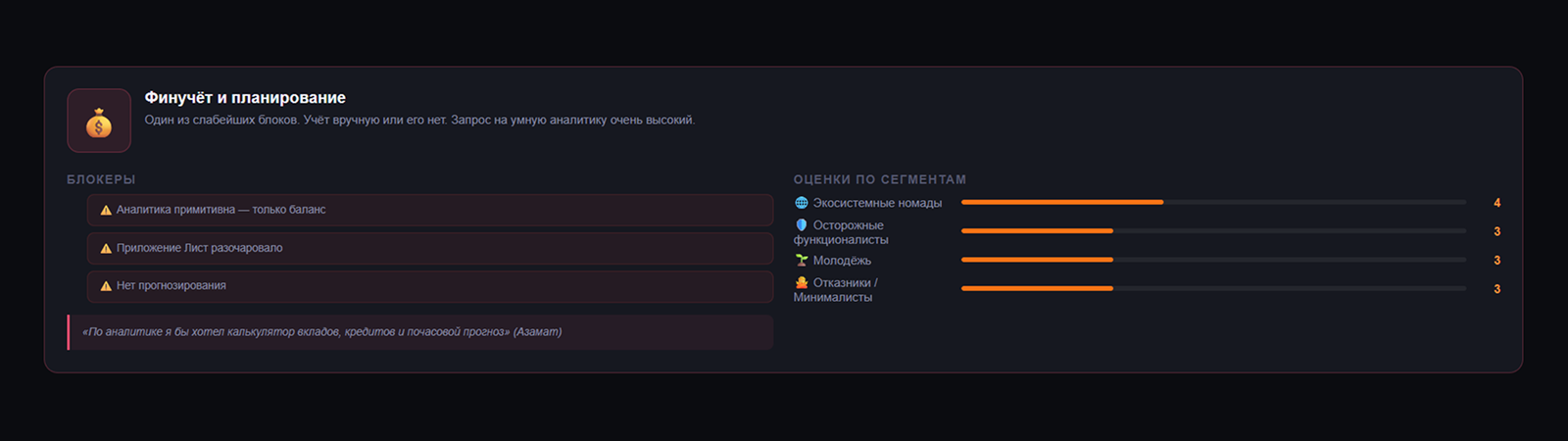

Key barriers: poor categorization and “digital shame”

Barrier 1: Algorithm blindness and the chaos of p2p transfers

The specificity of the Uzbekistan market is that a huge share of payments (at bazaars, beauty salons, taxis) still occurs via direct card-to-card transfers. To a banking algorithm, all these transactions look like “Transfers” or “Other.” As a result, at the end of the month, the user sees a chart where 60% of their spending occupies gray areas, making the entire analytics process meaningless.

Product insight: Ecosystems need to implement machine learning (ML) for contextual analysis of transfers. If a client sends the same amount to the same person every month with the note “for the apartment,” the system should offer to assign the “Rent” category to this recipient. It is also important to give users a convenient tool for mass reassignment of categories with swipes, so that the process of training the algorithm for oneself takes seconds, not minutes.

Barrier 2: Budget toxicity and the “digital shame” effect

Most financial tracking interfaces are designed in a way that visually punishes the user: red overspending numbers, warning push notifications about exhausted limits. This causes anxiety and guilt (“digital shame”) in the client. As a result, a psychological defense kicks in: the person simply stops visiting the analytics section so as not to ruin their mood.

Product insight: Interfaces must switch from a paradigm of “control and restrictions” to a paradigm of “encouragement and gamification.” Instead of highlighting overspending on coffee in red, an AI assistant should gently suggest: “You have already spent more than usual on restaurants, maybe we should transfer the rest of the limit to your vacation savings?” Implementing “Safe daily amount” widgets works much better than strict monthly budgets.

Behavioral models: micromanagers and avoiders

-

Neurotic micromanagers: Want to control every penny. They create custom tags, split receipts into different categories (for example, separating cat food from general groceries in a single supermarket receipt). For these users, exporting data to Excel/CSV for further work in their own spreadsheets is critically important.

-

Avoiding fatalists: Live paycheck to paycheck. They do not use PFM (Personal Financial Management) because they “already know there is little money.” They can only be drawn into the tracking section through micro-investments (rounding up balances on purchases) or automatic distribution of their salary into envelopes (utilities, loans, food) on the day it arrives.

How it looks in practice

The family budget of a Tashkent couple clearly shows the limits of banking analytics. Groceries for the week are bought at Chorsu — a transfer to the seller’s card; shoe repair, hairdresser, son’s tutor — also p2p. At the end of the month, the expense chart confidently reports: 60% — “Transfers.” For the algorithm, this is honest; for a human, it is useless.

The wife keeps an Excel spreadsheet in parallel, the husband “keeps it in his head.” Meanwhile, the app sends a push notification “You have exceeded your entertainment budget” due to an online cinema subscription — but fails to notice that a third of the salary goes to the same recipient every month for apartment rent. One interface gesture — “pin category to recipient” — would do more for trust in analytics than any chart redesign.

Why it matters

A bank that becomes the client’s main financial advisor will secure their loyalty forever. High-quality PFM allows the ecosystem to collect enriched data, which radically improves scoring models for issuing loans and installment offers.

FAQ

How to get people to use financial tracking?

Remove any manual labor from the process. Analytics should be built in the background, and the client should only receive ready-made, personalized insights (“This month you saved 50,000 soums on taxis”).

What to do with cash expenses?

It is impossible to fully integrate cash, but adding a simple “Add expense from wallet” widget right on the main screen partially solves the problem for disciplined users.

Why can’t we just copy foreign PFM solutions?

Western algorithms rely on card MCC codes: there, almost every expense goes through a terminal with a clear category. In Uzbekistan, a significant part of everyday payments are p2p transfers, which have no category. Without local models trained on such patterns, analytics remains blind.

Original source of the research: How Uzbekistanis track finances in banking ecosystems